Chorus One is now a part of Bitwise. Bitwise is a global, crypto-first asset manager with $11 billion+ in client assets and a diverse suite of investment solutions. Learn more about how Chorus One is growing as a part of Bitwise at onchain.bitwiseinvestments.com.

Most blockchains were built as shared infrastructure. Everyone using the network competes for the same resources, follows the same rules, and lives with the same constraints. That works well for open markets and trading applications. It creates problems for regulated financial institutions that need predictable costs, compliance controls, and the ability to decide who participates in their network.Avalanche was designed around a different premise. Rather than forcing all participants onto a single shared chain, it is a platform for creating purpose-built financial networks (called Avalanche L1s). A bank can operate its own network with its own rules and its own list of permitted participants. Each L1 has its own dedicated validators and does not share traffic or compete for resources with others, while remaining interoperable with the broader Avalanche ecosystem through Interchain Messaging (ICM).

Most blockchains were built as shared infrastructure. Everyone using the network competes for the same resources, follows the same rules, and lives with the same constraints. That works well for open markets and trading applications. It creates problems for regulated financial institutions that need predictable costs, compliance controls, and the ability to decide who participates in their network.

Avalanche was designed around a different premise. Rather than forcing all participants onto a single shared chain, it is a platform for creating purpose-built financial networks (called Avalanche L1s). A bank can operate its own network with its own rules and its own list of permitted participants. Each L1 has its own dedicated validators and does not share traffic or compete for resources with others, while remaining interoperable with the broader Avalanche ecosystem through Interchain Messaging (ICM).

Settlement on Avalanche is confirmed in under two seconds and cannot be reversed. A transaction is either pending or final. Transaction costs run at fractions of a cent following the Avalanche9000 upgrade in late 2024. This combination of speed, low cost, and customisability has made Avalanche a leading platform for institutions working on tokenisation, settlement, and payments.

On 17 March 2026, the SEC and CFTC jointly classified AVAX as a digital commodity, the same regulatory category as Bitcoin and Ether, as part of a broader 16-asset designation. This removes years of legal uncertainty and opens the door for institutional products such as ETFs and structured instruments. The classification is currently interpretive guidance, not permanent law. Congress is working to codify it through the CLARITY Act.

The Avalanche architecture

Avalanche is not a single blockchain. It has a primary network at its core containing three specialised chains, each built for a specific job. On top of that foundation, institutions can launch their own custom networks (Avalanche L1s) with their own rules, their own participants, and their own compliance logic.

The P-chain is the administrative layer. It keeps track of every validator on the network, manages who is staking, how much, and distributes rewards.

The X-chain handles the movement of assets. It is optimised for speed and low cost, designed specifically for transferring value rather than running complex logic.

The C-chain is where applications live. It is fully compatible with the Ethereum Virtual Machine, which means institutions and solidity developers can use familiar tools and deploy existing code without starting from scratch.

Custom networks sit below this foundation. Each one is isolated and operates under its own rules, but every transaction it processes is ultimately secured by the primary network above it. Two institutions can run entirely separate chains with no shared activity, and still settle transactions between them when needed. This is the feature that sets Avalanche apart from general-purpose blockchains: an institution's network only carries its own traffic, which means fees stay stable, throughput is predictable, and compliance logic is built into the protocol rather than added on later.

What major institutions are building on Avalanche

Entity

Category

Action

Date

Source

Visa

Payments

Added Avalanche for global stablecoin settlement (USDC, USDG, EURC)

Each deployment reflects a different set of requirements. Visa needed settlement infrastructure its global partners could plug into without operational complexity. Progmat needed a network that would satisfy Japanese regulators and connect domestic security tokens to international investors.

In each case the decision came down to the same practical criteria: fast settlement, predictable costs, customisable compliance controls, and EVM compatibility.

Staking: earning rewards on Avalanche

Avalanche is secured through proof-of-stake. Validators commit AVAX tokens to the network and earn rewards in return for providing that security. Stakers (also called delegators) can take part without running a node themselves, by locking up their AVAX with a validator they choose. Both earn rewards, paid in newly issued AVAX. As of June 15, 2026, a participant who stakes for the maximum one-year period earns a reward rate of approximately 6.3% per year.

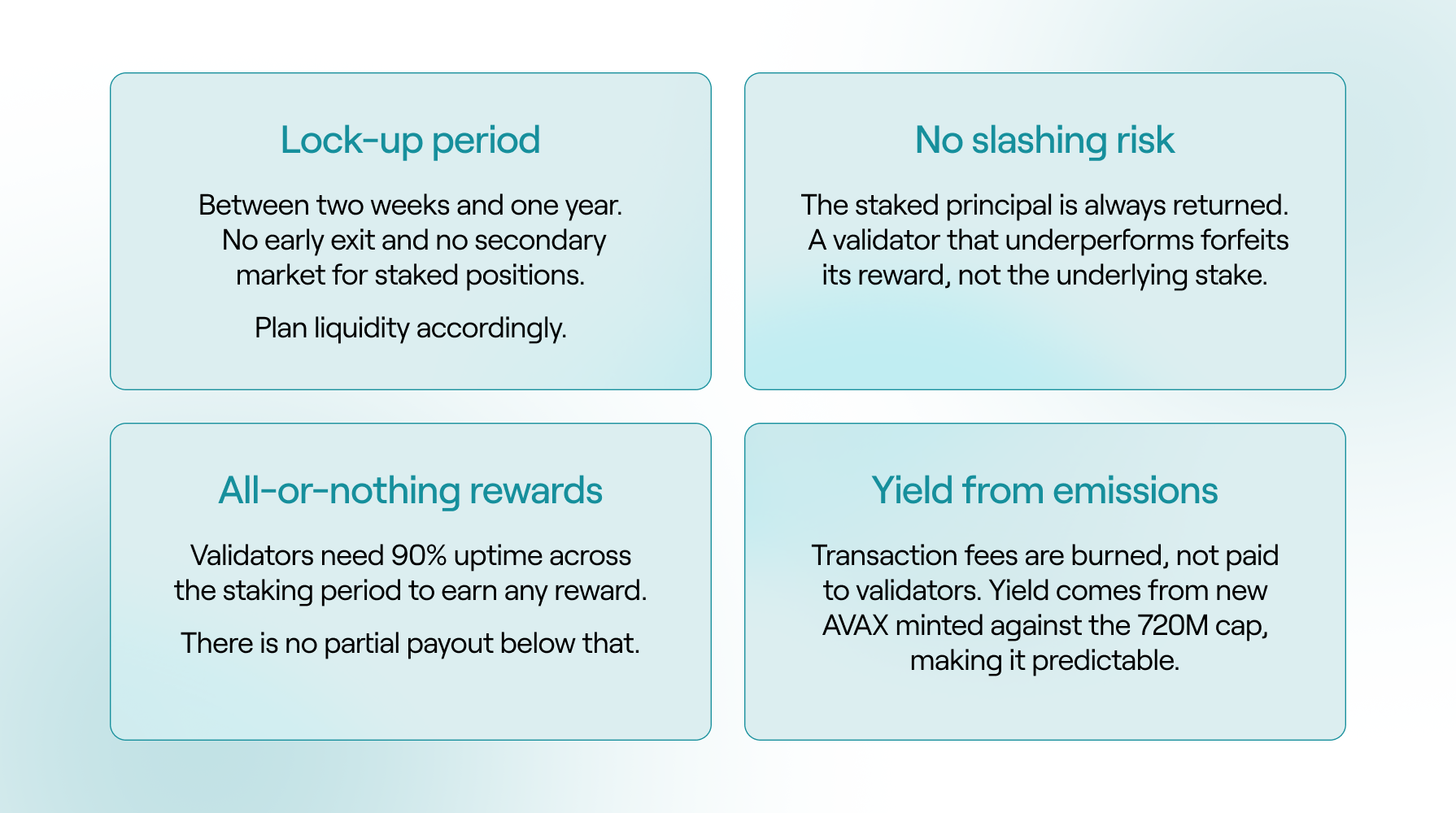

These rewards are not funded by transaction fees. Instead, the protocol issues new AVAX according to a fixed emission schedule, subject to a permanent maximum supply of 720 million tokens that cannot be exceeded. Separately, all transaction fees on Avalanche are burned, permanently removing those tokens from circulation and partially offsetting new issuance.

The reward rate is not fixed and changes over time. The protocol sets it automatically using a formula tied to how much AVAX has already been issued:

Rate = (Max Supply − Current Supply) ÷ Current Supply × Consumption Rate

Two elements drive the rate. First, as the circulating supply grows toward the 720 million cap, the "Maximum Supply − Current Supply" term shrinks, the pool of AVAX still available to be minted gets smaller and the reward rate gradually declines. Second, longer stakes earn more than shorter ones, up to a maximum consumption rate of 12% for a full one-year lock. The yield a staker actually keeps is lower than the headline rate, because validators charge a commission on the staking rewards.

The rate can be verified directly against the network. The only input that changes day to day is the current AVAX supply, which is read directly from the Avalanche blockchain. As of June 15, 2026, the supply was approximately 472.4 million AVAX, leaving 247.6 million to be issued before the 720 million cap. Applying the formula gives a nominal one-year reward rate of (247.6M ÷ 472.4M) × 12% ≈ 6.3%.

For institutional clients, the most direct route to earning staking rewards is through a professional validator operator. Bitwise Onchain Solutions operates validator infrastructure on Avalanche and manages this process on behalf of clients, handling uptime monitoring, infrastructure maintenance, and reward collection.

Disclosure:

The staking reward rate shown is derived from the Avalanche protocol's on-chain reward formula using the current AVAX supply of approximately 472.4 million AVAX, queried directly from the Avalanche P-Chain as of June 15, 2026, a maximum supply of 720 million AVAX, a maximum consumption rate of 12%, and a one-year staking period. Staking rewards are variable and not guaranteed. They may fluctuate or fall to zero depending on the total AVAX supply, the amount staked, protocol parameters, and validator performance, including the network's uptime requirements. For BAVA, any rewards earned accrue to the Fund and should not be taken as an indication of future performance.

The lock-up structure is the most important consideration for institutional clients. Staking durations on Avalanche range from a minimum of 2 weeks to a maximum of 1 year, and any duration within that window can be selected at the point of staking. Once committed, the position cannot be exited early and the parameters cannot be changed. The chosen duration should align with the client's liquidity planning accordingly.

This structure is likely to evolve. Avalanche has an active governance proposal (ACP-236) that would introduce continuous staking for validators, allowing them to remain staked indefinitely with automatic cycle renewals and optional reward compounding. Validators define their own cycle duration within the existing two-week to one-year range, and the position auto-renews at the end of each cycle. A validator can signal an exit at any point during a cycle, but capital remains locked until that cycle completes.

There is no slashing risk on Avalanche. The staked principal is fully protected at all times. If a validator fails to meet the uptime threshold, it simply does not earn rewards for that period. This is why choosing an operator with robust infrastructure and monitoring is important.

Three ways to access and gain exposure to Avalanche through Bitwise

Direct staking suits clients who hold AVAX and want full rewards exposure through dedicated infrastructure. Bitwise Onchain Solutions operates validators across more than 20 proof-of-stake networks and manages the full technical stack: uptime monitoring, reward collection, and reporting. The client retains ownership of the underlying tokens throughout.

The AVNB ETP was built specifically for clients who need daily liquidity. It holds AVAX in institutional cold-storage custody, stakes a portion of the holdings, and adds the staking rewards to the net asset value each day. Clients trade in and out on Deutsche Börse Xetra like any other exchange-traded product, without any lock-up period or operational complexity on their side. It has been listed since October 2025.

The BAVA ETF is the US-market equivalent. Once live, it will stake up to 70% of its holdings and pass the rewards directly to investors, making it one of the first rewards-bearing crypto ETFs in the United States. The gross expense ratio of 0.34% reflects Bitwise's commitment to offering the most cost-efficient access to AVAX staking available to US investors.

Why Bitwise

Bitwise brings together two capabilities that are rarely combined in one firm: deep blockchain infrastructure expertise and the institutional credibility of a regulated asset manager.

On the infrastructure side, Bitwise Onchain Solutions operates validators across more than 20 proof-of-stake networks, managing several billion dollars in staked assets. The team that built the non-custodial Ethereum staking tools now used by the Ethereum Foundation itself is part of Bitwise Onchain Solutions. That institutional pedigree is the same infrastructure powering our Avalanche validator operations.

On the product side, Bitwise has been building regulated access to digital assets since 2017, serving over 5,000 wealth managers, RIAs, family offices, and institutional investors. The AVNB ETP, the BAVA ETF, and our direct staking service are all expressions of the same belief: that institutional clients deserve professional, regulated access to blockchain infrastructure without having to manage the technical complexity themselves.

For clients looking to understand Avalanche, evaluate staking, or explore how blockchain infrastructure might fit into a broader portfolio, Bitwise Onchain Solutions is ready to go deeper.

Risks and Important Information

This material must be accompanied by a prospectus. To get this document for free, please visit bava.com/welcome.

The Bitwise Avalanche ETF (BAVA) is not suitable for all investors. An investment in BAVA is subject to a high degree of risk, has the potential for significant volatility, and could result in significant or complete loss of investment. BAVA is not an investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”) and therefore is not subject to the same protections as ETFs and mutual funds registered under the 1940 Act. An investment in BAVA is not a direct investment in Avalanche (AVAX-USD).

Shares of ETPs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The NAV may not always correspond to the market price of AVAX-USD and, as a result, Creation Units may be created or redeemed at a value that is different from the market price of the Shares. Authorized Participants’ buying and selling activity associated with the creation and redemption of Creation Units may adversely affect an investment in the Shares.

The amount of AVAX-USD represented by a Share will continue to be reduced during the life of the Fund due to the transfer of the Fund’s AVAX-USD to pay for the Sponsor’s management fee, and to pay for litigation expenses or other extraordinary expenses. This dynamic will occur irrespective of whether the trading price of the Shares rises or falls in response to changes in the price of AVAX-USD.

There is no guarantee or assurance that the Fund’s methodology will result in the Fund achieving positive investment returns or outperforming other investment products.

Investors may choose to use the Fund as a means of investing indirectly in AVAX-USD. Because the value of the Shares is correlated with the value of the AVAX-USD held by the Fund, it is important to understand the investment attributes of, and the market for, AVAX-USD.

AVAX-USD Risk. There are significant risks and hazards inherent in the AVAX-USD market that may cause the price of AVAX-USD to fluctuate widely. The Fund’s AVAX-USD may be subject to loss, damage, theft or restriction on access. Investors considering a purchase of Shares should carefully consider how much of their total assets should be exposed to the AVAX-USD market, and should fully understand, be willing to assume, and have the financial resources necessary to withstand the risks involved in the Fund’s investment strategy.

Liquidity Risk. The market for AVAX-USD is still developing and may be subject to periods of illiquidity. During such times it may be difficult or impossible to buy or sell a position at the desired price. Possible illiquid markets may exacerbate losses or increase the variability between the Fund’s NAV and its market price. The lack of active trading markets for the Shares may result in losses on investors’ investments at the time of disposition of Shares.

Regulatory Risk. Future and current regulations by a U.S. or foreign government or quasi-governmental agency could have an adverse effect on an investment in the Fund.

Blockchain Technology Risk. Certain of the Fund’s investments may be subject to the risks associated with investing in blockchain technology. The risks associated with blockchain technology may not fully emerge until the technology is widely used. Blockchain systems could be vulnerable to fraud, particularly if a significant minority of participants colluded to defraud the rest. Because blockchain technology systems may operate across many national boundaries and regulatory jurisdictions, it is possible that blockchain technology may be subject to widespread and inconsistent regulation.

Staking Risk. The Trust intends to implement a staking program under which a significant portion of the Trust’s AVAX-USD will be staked. While staking AVAX-USD offers the potential to earn rewards in the form of additional AVAX tokens, it also exposes the Trust to several risks, such as loss of rewards, slashing penalties, and operational uncertainties. Staking activities could impair the ability to satisfy redemption orders on a timely basis.

Nondiversification Risk. The Fund is nondiversified and will hold a single issue. As a result, a decline in the market value of a particular issue held by the Fund may affect the Fund’s value more than if it invested in a larger number of issuers.

Recency Risk. The Fund is recently organized, giving prospective investors a limited track record on which to base their investment decision. If the Fund is not profitable, the Fund may terminate and liquidate at a time that is disadvantageous to Shareholders.

Bitwise Investment Advisers, LLC serves as the sponsor of the Fund. Foreside Fund Services, LLC serves as the Marketing Agent for AVAX, and is not affiliated with Bitwise Investment Advisers, LLC, Bitwise, or any of its affiliates.

Nothing herein constitutes investment, legal, tax or accounting advice, nor a recommendation to

participate in any staking activity. Clients retain full discretion over all decisions relating to digital assets and staking participation.

Crypto asset trading requires knowledge of crypto asset markets. In attempting to profit through crypto asset trading, you must compete with traders worldwide. You should have appropriate knowledge and experience before engaging in substantial crypto asset trading. Crypto asset trading can lead to large and immediate financial losses. Under certain market conditions, you may find it difficult or impossible to liquidate a position quickly at a reasonable price.

The opinions expressed represent an assessment of the market environment at a specific time and are not intended to be a forecast of future events, or a guarantee of future results, and are subject to further discussion, completion and amendment. The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice, or investment recommendations. You should consult your accounting, legal, tax or other advisors about the matters discussed herein.

Staking is provided by Attestant Ltd. Doing business as “Bitwise Onchain Solutions” (“BOS”)

.png)

.png)