Chorus One is now a part of Bitwise. Bitwise is a global, crypto-first asset manager with $11 billion+ in client assets and a diverse suite of investment solutions. Learn more about how Chorus One is growing as a part of Bitwise at onchain.bitwiseinvestments.com.

DeFi Curators in 2025: Navigating Chaos, Building Resilience

Over the past year, the role of the DeFi curator, once a niche function in lending markets, has evolved into one of the most systemically important positions in the on-chain economy. Curators now oversee billions in user capital, set risk parameters, design yield strategies, and determine what collateral is considered “safe.”

DeFi Curators in 2025: Navigating Chaos, Building Resilience

Kam Benbrik

Yannick Socolov

December 2, 2025

•

18 min read

December 2, 2025

•

5 min read

Intro

Over the past year, the role of the DeFi curator, once a niche function in lending markets, has evolved into one of the most systemically important positions in the on-chain economy. Curators now oversee billions in user capital, set risk parameters, design yield strategies, and determine what collateral is considered “safe.”

But DeFi learned an expensive lesson: many curators weren’t actually managing risk; they were cosplaying it.

A Balancer exploit, a cascading stablecoin collapse, and liquidity crises across top vaults forced the industry to confront an uncomfortable truth: the system worked as designed, but the people setting the guardrails did not.

The DeFi Curator Market Today

As DeFi evolves, risk management and capital efficiency are becoming modular and specialized functions. A new category of entities, called curators, now design and manage on-chain vaults, marking a major shift in liquidity management since automated market makers. The concept of the curator role was pioneered and formalized by Morpho, which externalized risk management from lending protocols and created an open market for curators specializing in vault strategy and risk optimization. This new standard has since been adopted across DeFi, making curators fundamental for managing vaults and optimizing risk-adjusted returns for depositors.

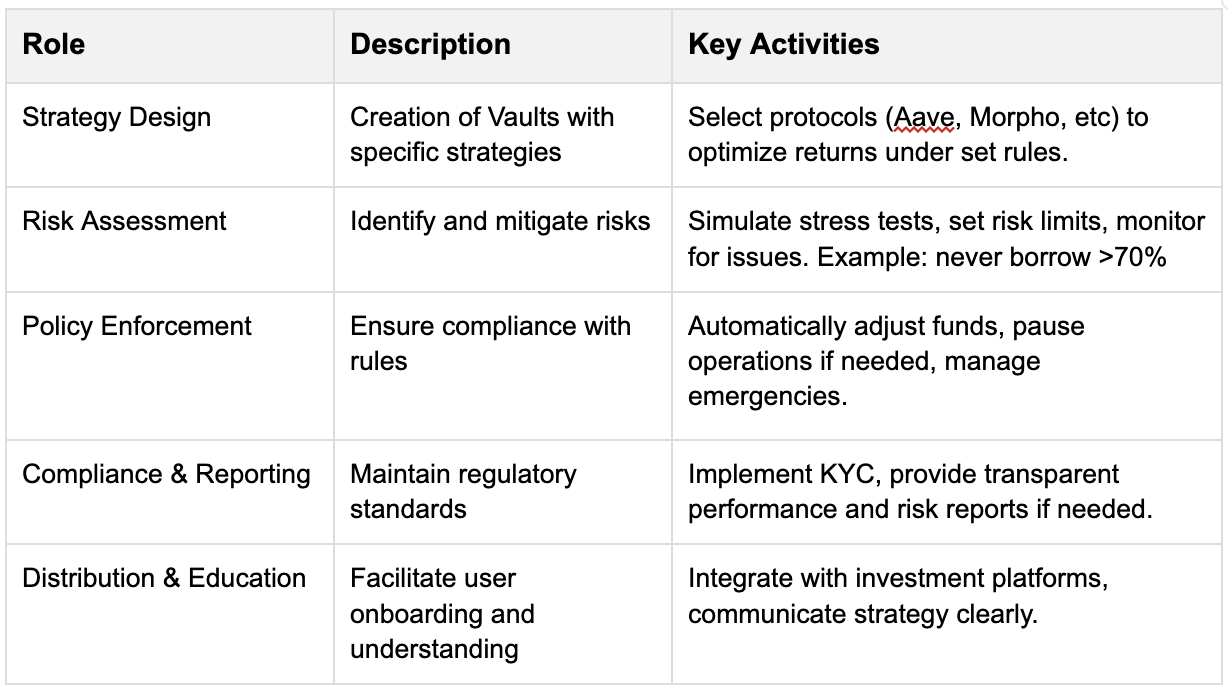

Core Responsibilities of Curators

A curator is a trusted, non-custodial strategist who builds, monitors, and optimizes on-chain vaults to deliver risk-adjusted yield for depositors. They design the rules, enforce the limits, and earn performance fees on positive results.

Here’s an overview of the core roles and activities associated with a curator:

Activities associated with a curator

Market Structure

The curator market in DeFi has rapidly grown from $300 million to $7 billion in less than a year, reflecting a 2,200% growth. This surge marks a key milestone in the development of risk-managed DeFi infrastructure. The increase is driven by new lending protocols adopting the vault architecture, institutional inflows, the rise of stablecoins, clearer regulations, and growing trust in curators like Stakehouse or Gauntlet.

While we’re still in the “wild west” era of DeFi as recent events have shown, curators are a first step to introduce more isolated and essential risk controls, making on-chain yields more predictable, compliant, and secure for users. This has also enabled companies to introduce “earn”-type of products to their users in a simplified way.

Key metrics:

Over half of the TVL value managed by curators is on Ethereum, reflecting its deep money market liquidity and continued DeFi dominance. Although still early, top curators have captured significant market share, with the top five controlling around 43%. Much of their success comes from their role on Morpho, while other protocols like Kamino v2 and Euler are still growing with similar models.

With recent events, the curators landscape got reshuffled a bit. Gauntlet took over the top spot from Steakhouse and is managing approximately $1.88 billion in TVL. Previously, Steakhouse’s focus on stablecoin-oriented strategies had allowed it to outpace competitors such as Gauntlet and MEV Capital. Steakhouse now manages $1.26 billion, and also holds a particularly strong position within Kamino on Solana, capturing 20% market share ($295M TVL), though it remains absent from restaking-focused protocols such as Symbiotic.

The business model of DeFi curators is primarily driven by performance fees, earned as a percentage of the yield or profits generated by the vaults they manage. This structure effectively aligns incentives, as curators are rewarded for optimizing returns while maintaining prudent risk management. Curators also work directly with B2B partners in building special-purpose vaults where pricing and revenue share is decided between the participating parties.

Some curators have adopted a 0% performance fee structure on their largest vaults to attract liquidity and strengthen brand recognition (for example, Steakhouse’s USDC vault). Current revenue data available on DeFiLlama provides a good indicator for assessing the earnings and relative performance of active curators.

DeFi’s Really, Really Bad Week

It began when Balancer v2 stable pools were exploited on November 3, 2025, with a precision rounding bug in the stable swap math that let an attacker drain about 130 million dollars. Seeing a near five year old, heavily audited protocol fail triggered a broad risk reset and reminded everyone that DeFi yield carries real contract risk. Around the same time, Stream Finance disclosed that an external fund manager had lost about 93 million dollars of platform assets. Stream froze deposits, and its staked stablecoin xUSD depegged violently toward 0.30 dollars.

xUSD was widely rehypothecated as collateral. Lenders and stablecoin issuers had lent against it or held it in backing portfolios, in some cases with highly concentrated exposure. When xUSD’s backing came into question, pegs had to be defended, positions were unwound, and exits were gated. What started as a few specific failures became a system wide scramble for liquidity, which is what eventually showed up to users as queues, withdrawal frictions, and elevated rates across curator vaults and lending protocols.

Liquidity Crunches on Vaults

We saw large liquidity crunches on Morpho after the xUSD / Stream Finance blowup. On Morpho, only one of roughly 320 MetaMorpho vaults (MEV Capital's) had direct exposure to xUSD, resulting in about $700,000 in bad debt. However, the shock raised ecosystem-wide risk aversion, with many lenders wanting to withdraw at once.

These liquidity crunches were mainly driven by simultaneous withdrawals colliding with Morpho's isolated-market design. MetaMorpho vaults like Steakhouse USDC aggregate UX, not liquidity. Each vault operates with isolated lending markets and no shared liquidity. Each market has a cap, a LTV limit, and a utilization level that tracks how much cash is already lent out.

When many depositors rushed to withdraw, the only immediately available cash was the idle balance in those specific markets. That idle cash got used up first, utilization hit 100%, and withdrawals moved into a queue. As utilization climbed, the interest rate curve ramped up, spiking as high as 190%, to incentivize borrowers to repay or get liquidated. While that released cash, it doesn't happen instantly. Borrowers need to source funds or liquidations need to clear. Until that flow returns cash to the vault's underlying markets, withdrawals remain slow because there is no shared pool to tap outside the vault's configured markets.

Crucially, even 'safe' USDC vaults without xUSD exposure, like those managed by Steakhouse or Gauntlet briefly became illiquid, out of caution rather than losses. The fragmented liquidity meant funds couldn't be pulled from some global pool, resulting in a classic timing mismatch: immediate redemption demand versus the time needed for borrowers to de-lever and for the vault to pull funds back from its underlying markets. Even so, these vaults recovered within hours, and overall, 80% of withdrawals were completed within three days.

As a random guy on Twitter pointedly said: “It appears that the Celsius/BlockFi’s of this cycle are DeFi protocols lending to vault managers disguised as risk curators”.

The incident demonstrated that Morpho's design worked as intended: isolation contained the damage to one vault, curator decisions limited broader exposure, and the system managed acute stress without breaking. However, it also revealed the tradeoff inherent in the design—localized liquidity can drain quickly even when actual losses are minimal and contained.

Protocol Design Choices (Aave vs Morpho)

Aave and Morpho both enable borrowing and lending, but they differ in how they manage risk and structure their markets.

With Aave, the protocol manages everything: which assets are available, the risk rules, and all market parameters. This makes Aave simple to use. Depositors provide capital to shared pools without making individual risk decisions. This setup ensures deep liquidity, fast borrowing, and broad asset support. However, this “one-size-fits-all” model means everyone shares the same risk. If Aave’s risk management or asset selection fails, all depositors may be affected, and users have limited ability to customize their risk exposure.

Morpho, on the other hand, decentralizes risk management by allowing independent curators (like Gauntlet or Steakhouse) to create specialized vaults. Each vault has its own risk parameters, such as different collateral requirements, liquidity limits, or liquidation rules. Lenders and borrowers choose which vaults to use based on their risk appetite. This provides much more flexibility, allowing users to select safer or riskier strategies.

However, this flexibility also leads to fragmented liquidity. Funds are spread across many vaults, and users must evaluate each vault’s risks before participating. For non-experts, this can be challenging, and it can occasionally result in lower liquidity or slower withdrawals during volatile market conditions.

What Should Have Been Done Differently?

While the Balancer hack is out of the control of any curator and was hard to foresee, xUSD is a different story. Basic risk hygiene would have gone a long way. If curators had treated xUSD as a risky credit instrument rather than “dollar-equivalent collateral,” most of the bad debt, queues, and forced deleveraging would have been materially smaller. Curators need to step their game up and there is a lot of room for improvement…

Future Directions and Market Gaps in the Curator Role

Over the coming years, resolving gaps in regulatory clarity, risk metrics, distribution access, and technical interoperability will transform curators from crypto-native specialists into fully licensed, ratings-driven infrastructure that channels institutional capital into on-chain yield with similar standards and scale of traditional asset managers.

Regulatory Landscape

The curator market currently operates in a regulatory grey area. Curators do not hold assets or control capital directly, but their work (configuring vaults and tracking performance) closely resembles activities of regulated investment firms/advisors. At the moment, none of the major curators are licensed. Yet to serve banks and RIAs, curators will need investment advisor registration, KYC capabilities, and institutional custody integration—the compliance stack that crypto-native players deliberately avoid.However, the market is slowly moving toward regulated infrastructure, as shown by Steakhouse’s partnership with Coinbase Institutional, the tokenized Treasury efforts of Ondo and Superstate or Société Générale announcing depositing into a Morpho. Under current U.S. and EU rules, curators who earn performance fees or promote yield-generating products may eventually fall under investment advisory regulations. This creates both a compliance risk and a first-mover opportunity: a regulated curator could define new governance standards, attract institutional investors, and speed up the market’s formalization.

No Unified Risk Framework

One gap in the DeFi curator market is the absence of a standardized risk taxonomy. Today, every curator invents its own subjective labels: “Prime”, “Core”, “High-Yield” or “Aggressive” with no shared definitions, no comparable metrics, and no regulatory acceptance. There have been attempts by a number of players, such as Exponential, Credora (acquired by Restone), and Synnax, to create a unified standard for risk ratings, but no universal standard has been accepted by the space yet.This fragmentation blocks advisors from building compliant portfolios and prevents institutions from scaling allocations. In traditional finance, the Big 3 credit rating agencies (Moody’s, S&P, Fitch) generate over $6 billion annually by applying universal, transparent ratings to $60 trillion in debt. DeFi needs the same: AAA/BBB ratings with hard rules on parameters such as collateral types, oracle design, initial and liquidatable LTVs, and liquidity thresholds.Without it, curated TVL stays siloed and institutional inflows can remain limited. The first player to deliver a Moody’s-grade rating with Standard labels, Transparent methodology and Regulatory acceptance has the opportunity to own the category and unlock the next $100 billion in advisor-driven deposits.

Distribution Remains Bottlenecked

The market is still bottlenecked by crypto-native brands. Curators like Steakhouse and MEV Capital dominate TVL with battle-tested strategies, but they lack the institutional credibility, regulatory wrappers, and advisor relationships that RIAs and private banks demand. This leaves billions in potential deposits stranded in wallets or CEXs, unable to flow seamlessly into curated vaults. In TradFi, asset managers like BlackRock route trillions through established RIA platforms, wealth desks, and brokerage channels. DeFi has not a lot of equivalents yet: The Coinbase x Morpho cbBTC partnership is the exception proving the rule, and shows early promising signs that with sufficient track record and credibility, institutions and platforms with distribution are willing to tap into DeFi-native strategies. When infrastructure connects, billions flow. We need more of it. Custodian APIs that let advisors allocate client funds on-chain, wealth platform integrations, etc. Société Générale's digital asset arm, SG-FORGE, selected Morpho specifically because its architecture solves the problem of finding a regulated, compliant counterparty for on-chain activities. The curator who can build the "click-through" infrastructure that turns any compliant vault into an advisor-native product will unlock the next $50 billion in institutional AUM.

Technical Fragmentation

DeFi curators face major technical fragmentation. Each platform (such as Morpho or Kamino) requires its own custom code, dashboards, and monitoring tools. Managing a single vault across multiple platforms means rebuilding everything from scratch, much like opening separate bank accounts with no shared infrastructure. This slows growth, increases costs, and limits scale. What's missing: one system to configure all vaults. Set position limits once, deploy to Morpho and Kamino automatically. Build for one platform, launch on ten.What the market needs is a unified engine that works across all platforms: configure it once, apply consistent rules, and manage every vault through the same system.

Conclusion

The recent failures proved two things simultaneously:

DeFi’s architecture is resilient: Isolation worked. Losses were contained. Liquidity returned. The system bent but did not break.

DeFi’s risk culture is not resilient: Curators mispriced collateral, mis-sized positions, and treated credit-like assets as stablecoins. The failures were not black swans, but predictable results of weak standards.

If curators want to handle institutional capital, they must evolve from clever yield optimizers into true risk managers with:

hard collateral constraints

standardized ratings

transparent reporting

institutional compliance

distribution-ready infrastructure

The next $50–$100B of on-chain yield will flow to curators who look less like DeFi power users and more like regulated asset managers. Conservative risk frameworks. Scalable distribution. Institutional compliance.

The curator role isn't disappearing. It's professionalizing.