Chorus One is now a part of Bitwise. Bitwise is a global, crypto-first asset manager with $11 billion+ in client assets and a diverse suite of investment solutions. Learn more about how Chorus One is growing as a part of Bitwise at onchain.bitwiseinvestments.com.

Solana remains one of the fastest and most adopted blockchains in the crypto ecosystem. In this context, we view Alpenglow as a bold and necessary evolution in the design of Solana’s consensus architecture.

Alpenglow’s higher fault tolerance (40% vs 33%) comes at a modest and bounded cost when compared with Solana PoH.

A higher number of epochs increases the effects of compounding rewards up to the dominance of disinflation.

The possibility to decrease slot time can lead to

a ~38% reduction in MEV rewards from arbitrage

a ~24% reduction in MEV rewards from sandwiches

Lower grace period and reduced revenues from MEV may eventually push for geographical concentration of stake.

Shreds propagation design from relay may introduce disparities between validators, imposing a latency tax on small stake.

The choice for the overprovisioning of shreds (indirectly number or relays and shreds needed to reconstruct a slice), as presented in the original paper, still brings high block failure. Varying this parameters may have effects on network bandwidth.

The current design for message propagation is prone to Authenticate DDoS attacks.

PoH removal can potentially lead to a higher share of failed transactions landing on-chain.

The reward mechanism requires careful design, as it can be easily gamed if not properly constrained.

Alpenglow introduces randomness in rewards accrued per epoch. A careful design is required in order to avoid asymmetry between different stake shares.

1. Introduction

Solana remains one of the fastest and most adopted blockchains in the crypto ecosystem. In this context, we view Alpenglow as a bold and necessary evolution in the design of Solana’s consensus architecture.

Our position is fundamentally in favour of this shift. We believe that Alpenglow introduces structural changes that are essential for unlocking Solana’s long-term potential. However, with such a radical departure from the current Proof-of-History (PoH) based system, a careful and transparent analysis of its implications is required.

This document is intended as a complement to existing reviews. Rather than offering summary of the Alpenglow consensus, well covered in resources like the Helius article, our aim is to provide a rigorous peer review and a focused analysis of its economic incentives and potential trade-offs. Our goal is to provide a critical perspective that informs both implementation decisions and future protocol research.

The article is structured as follows. In Sec. 2 we go straight into the Alpenglow whitepaper to provide a peer review. Precisely, in Sec. 2.1 we analyze the less than 20% Byzantine stake assumption. In Sec. 2.2 we explore the effects of epochs on rewards compounding. In Sec. 2.3 we assess the implication of reduced slot time on MEV. In both Sec. 2.4 and 2.5 we study some implications of propagation design as presented in the original paper. In Sec. 2.6 we explore the possibility to perform Authenticated DDoS attack on the network. In Sec. 2.7 we assess some network assumptions and systemic limitations. Finally, in Sec. 2.8 we discuss some implications of PoH removal.

In Sec. 3 we explore some implications that arise from how tasks are rewarded under Alpenglow. Precisely, in Sec. 3.1, 3.2 and 3.3 we present three ways in which a sophisticated node operator can game the reward mechanisms. In Sec. 3.4 we assess the effects of randomness on rewards.

2. Protocol Review

In this section, we take a critical look at the Alpenglow consensus protocol, focusing on design assumptions, technical trade-offs, and open questions that arise from its current formulation. Our intent is to highlight specific areas where the protocol’s behaviour, performance, or incentives deserve further scrutiny.

Where relevant, we provide probabilistic estimates, suggest potential failure modes, and point out edge cases that may have meaningful consequences in practice. The goal is not to undermine the protocol, but to contribute to a deeper understanding of its robustness and economic viability.

2.1 - The 5f+1 fault tolerance

Alpenglow shifts from a 33% Byzantine tolerance to a 20% in order to allow for fast (1 round) finalization. While the 5f+1 fault tolerance bound theoretically allows the system to remain safe and live with up to 20% Byzantine stake, the assumption that Byzantine behaviour always takes the form of coordinated, malicious attacks is often too narrow. In practice, especially in performance-driven ecosystems like Solana, the boundary between rational misbehaviour and Byzantine faults becomes blurred.

Validators on Solana compete intensely for performance, often at the expense of consensus stability. A prominent example is the use of mod backfilling. While not explicitly malicious, such practices deviate from the intended protocol behaviour and can introduce systemic risk.

This raises a key concern: a nontrivial fraction of stake, potentially exceeding 20%, can engage in behaviours that, from the protocol’s perspective, are indistinguishable from Byzantine faults. When performance optimization leads to instability, the classical fault threshold no longer guarantees safety or liveness in practice.

Alpenglow models this possibility by allowing an additional 20% of the stake to be offline. This raises the resistance to 40% of the stake, being more aligned with a real implementation of a dynamical and competitive distributed system.

An essential question arising from the 5f+1 fault-tolerance threshold in Alpenglow is whether the current inflation schedule adequately compensates for security. To address this, we use the same formalism developed in our SIMD-228 analysis.

The primary task is to determine under what conditions the overpayment statement holds for a 20% Byzantine + 20% crashed threshold. To assess if the current curve is prone to overpayment of security, we need to study the evolution of the parameters involved. This is not an easy task, and each model is prone to interpretation.

The model is meant to be a toy-model showing how the current curve can guarantee the security of the chain, overpaying for security based on different growth assumptions. The main idea is to assess security as the condition

where the profit is estimated assuming an attacker can drain the whole TVL. Precisely, since the cost to control the network is >60% of total stake S (Alpenglow is 20% Byzantine + 20% crash-resistant), we have that the cost to attack is 0.6 × S, and the profit is the TVL. In this way, the chain can be considered secure provided that

In our model, we consider the stake rate decreasing by 0.05 following the equivalent of Solana PoH 150 epochs, based on the observation done in the SIMD-228 analysis. We further consider a minimum stake rate of 0.33 (in order to compare with the SIMD-228 analysis), a slot time of 400ms, 18,000 slots per epoch, and we fix the TVL to be DeFi TVL. We also assume 0 SOL as burn rate since we will not have vote transactions anymore, and we don’t know how many transactions Solana will handle per slot under Alpenglow.

It is worth noting that, these parameters are based on empirical data and what is used as default in the Alpenglow withepaper (page 42, Table 9).

The first case we want to study is when TVL grows faster than SOL price. We assumed the following growth rates:

SOL price growth of 20% a year - in 10 years, this means 1 SOL ~ $866.84

TVL growth of 62% a year in the first 4 years and 10% growth in the following years - this means Solana DeFi will reach Ethereum TVL in 4 years

The dynamical evolution obtained as an outcome of these assumptions is depicted below.

With the assumed growth rate, the current inflation schedule is projected to maintain adequate security for slightly more than two years. Notably, this has no real difference when compared to the timeline derived from the same growth scenario applied to the current Solana PoH implementation.

It is worth reiterating that the toy model presented here is a simplified parametrization of reality. The goal is not to precisely determine whether the current inflation schedule leads to overpayment or underpayment for security. Rather, it serves to quantify the impact of lowering the takeover threshold from 66% to 60% of stake under Alpenglow.

This shift implies that an adversary must control a smaller fraction of the stake to compromise the system, thereby reducing the cost of an attack. As the model shows, even a 6 percentage point increase may appear substantial, but in a scenario with fast TVL growth, the system shows virtually no difference compared to the PoH consensus. This suggests that Alpenglow’s higher fault tolerance comes at a modest and bounded cost, at least under optimistic growth assumptions.

As in the PoH scenario, if we assume SOL’s price growth rate surpasses the growth rate of the network’s TVL, the current inflation schedule would lead to approximately ten years of overpayment for network security, cfr. SIMD-228: Market Based Emission Mechanism.

2.2 - Effects of Epochs on Inflation

Alpenglow and the current Solana PoH implementation differ in the frequency of reward compounding. While both mechanisms eventually use a similar inflation curve, they distribute and compound rewards at vastly different rates: a lower number of slots per epoch increases the number of epochs per year in Alpenglow, compared to Solana PoH.

This difference in epoch definition (and slot time) has a direct impact on the effective APY received by validators. Even when the nominal inflation rate is identical, more frequent compounding leads to higher APY, due to the exponential nature of compound interest.

Formally, for a given nominal rate r and compounding frequency n, the APY is given by:

With Alpenglow’s much higher n, this yields a strictly larger APY than PoH under equivalent conditions. In the limit as n -> ∞, the APY converges to e^r-1, the continuously compounded rate. Alpenglow therefore approximates this limit more closely, offering a higher geometric growth of rewards.

This behaviour is illustrated in the figure above, which compares the compounded returns achieved under both mechanisms across different stake rates. The difference is particularly noticeable over short to medium time horizons, where the higher compounding frequency in Alpenglow yields a tangible compounding advantage. However, as the projection horizon extends, e.g., over 10 years, the difference becomes increasingly marginal. This is due to two effects: first, the declining inflation rate reduces the base amount subject to compounding; second, the PoH system's less frequent compounding becomes less disadvantageous once inflation levels off. In long-term projections, the frequency of compounding is a second-order effect compared to the shape of the inflation curve and the total staking participation.

2.3 - Network Delay and MEV

A central design parameter in Alpenglow is the network delay bound Δ, which defines the maximum time within which shreds and votes are expected to propagate for the protocol to maintain liveness. In practice, Alpenglow reduces Δ to nearly half of Solana’s current grace period (~800 ms), aiming for faster finality and tighter synchronization.

It is worth mentioning that, Alpenglow will not directly lower the slot time, which will be kept fixed at 400ms. However, Alpenglow makes lower slot time more reliable, meaning that in the future slot time can be lowered.

2.3.1 - Effects on Arbitrage

In this section, we consider the impacts of reducing network delay on arbitrage opportunities. We know, from Milionis et al, that the probability of finding an arbitrage opportunity between 2 venues is given by

where λ is the Poisson rate of block generation (i.e. the inverse of mean block time, Δt = λ⁻¹, γ is the trading fee, and σ is the volatility of the market price’s geometric Brownian motion.

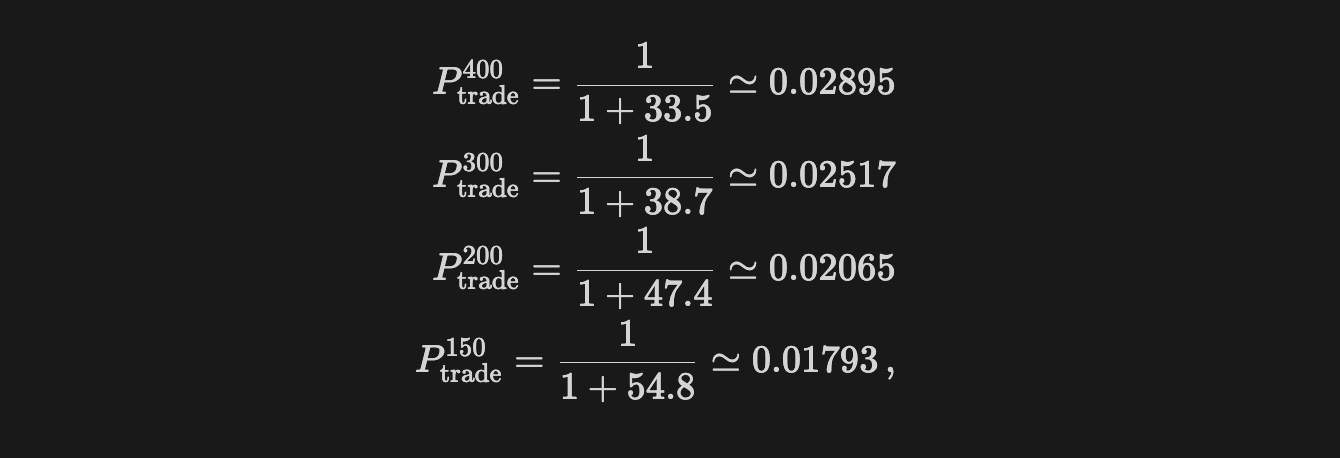

From the trade probability, it is clear that reducing block time from 400ms also reduces the probability of finding an arbitrage opportunity within a block. Precisely, if we assume a daily volatility of 5% (σₛₑcₒₙd ~ 0.02%) and a fee γ = 0.3% we get

which represents a ~38% reduction on the probability we find a profitable arb.

The reduction on arbitrage probability clearly affects final rewards. Precisely, Corollary 2 of Milionis et al provides a closed form for arbitrage profit normalized by pool value V(p) in the case of a CPMM,

Indeed, by taking the ratio between the arbitrage profits in the case of different block times, we get

This means that the revenue from the same arbitrage opportunity decreased by ~38.2%. The same result still holds if the DEX implements concentrated liquidity, we have a similar result that can be obtained using Theorem 3 of Milionis et al (Asymptotic Analysis), which leads to

where y*(p) = –L / (2√p) within the price range [pa, pb].

It is worth noting that the functional form is a consequence of the fact that liquidity is concentrated within a price range. If the market price or pool price exists in this range, arbitrage profits are capped, as trades can only adjust to p_a or p_b. This reduces the magnitude of arbitrage profits compared to CPMMs for large mispricing.

It follows that the arb difference is dependent just from Ptrade, that is

which is consistent with the CPMM result.

2.3.2 - Effects on Timing Games

A direct consequence of reducing the “grace period” to approximately 400 ms, combined with the associated effects on arbitrage profitability, is the emergence of timing games. Sophisticated node operators are incentivized to engage in latency-sensitive strategies that exploit their physical proximity to the cluster. In particular, by positioning infrastructure geographically close to the majority of validators, they can receive transactions earlier, selectively delay block propagation, and increase their exposure to profitable MEV opportunities.

This behaviour may lead to a feedback loop: as Δ shrinks, the value of low-latency positioning increases, pushing operators to concentrate geographically, thereby undermining the network’s decentralization. While such latency-driven optimization already occurs under PoH, Alpenglow’s smaller Δ significantly amplifies its economic and architectural consequences.

To assess the impact of block time on sandwich attack profitability in a blockchain, we derive the probability p(tau) of successfully executing a sandwich attack, where tau is the slot time (time between blocks).

A sandwich attack involves an attacker detecting a victim’s transaction that impacts an asset’s price, submitting a front-run transaction to buy before the victim’s trade, and a back-run transaction to sell afterward, exploiting the price movement.

Transactions arrive at the mempool as a Poisson process with a blockchain transaction rate of Λ = 1,000 TPS, yielding a per-block rate λ = Λ·τ. Blocks are produced every τ seconds. The victim’s transaction is one of these arrivals, and we consider its arrival time tᵥ within the interval [0, τ]. Conditional on at least one transaction occurring in [0, τ], the arrival time of the first transaction is uniformly distributed over [0, τ]. Indeed, the Poisson process’s arrival times, conditioned on N(τ) = k ≥ 1, result in k arrival times T₁, T₂, …, Tₖ, which are distributed as independent uniform random variables on [0, τ]. If the victim’s transaction is any one of these arrivals, chosen uniformly at random, its arrival time tᵥ is equivalent to a single uniform random variable on [0, τ], so tᵥ ~ Uniform[0, τ].

The attacker detects the victim’s transaction and prepares the attack with latency d, submitting front-run and back-run transactions at time tᵥ + d, where tᵥ is the victim’s arrival time. We focus on the single-block sandwich, where all transactions are included in the same block in the correct order, ensured by high priority fees or Jito tips.

For a successful single-block sandwich, the attacker must submit the front-run and back-run transactions at tᵥ + d, and all three transactions (front-run, victim, back-run) must be included in the block at τ. The submission condition is tᵥ + d ≤ τ.

Since tᵥ ~ Uniform[0, τ], the probability density function is f(tᵥ) = 1 / τ, and the probability of submitting in time is

If τ < d, then tᵥ + d > τ for all tᵥ ∈ [0, τ], making submission impossible, so P(tᵥ ≤ τ − d) = 0. The back-run is submitted at tᵥ + d + δ, where δ is the preparation time for the back-run. Assuming δ ≈ 0 (realistic for optimized MEV bots), both transactions are submitted at tᵥ + d, and the same condition applies. We assume the block has sufficient capacity to include all three transactions, and the attacker’s fees/tips ensure the correct ordering (front-run, victim, back-run) with probability 1. Thus, the probability of a successful sandwich is:

This linear form arises because the uniform distribution of tᵥ implies that the fraction of the slot interval where tᵥ ≤ τ − d scales linearly with τ − d. The profitability of a sandwich attack can be written as

where ε is the slippage set from the victim’s transaction, V is the victim’s volume, and F is the fee. To quantify the relative change when reducing block time from τ₄₀₀ = 0.4 s to τ₁₅₀ = 0.15 s, we can compute

since the profit per executed sandwich is independent of block time. If we assume d = 50 ms, we get

indicating that the profit with a slot time of 400 ms is 31.25% higher than the profit with a slot time of 150 ms (or equivalently, we have a 23.8% reduction in sandwich profits with Alpenglow).

Before ending the section, it is worth mentioning that, in real cases, sandwich attacks suffer from interference (e.g., from competitors). Precisely, on Solana, transactions are processed in a loop during the slot time. This means that, if the loop lasts for tₗₒₒₚ, there is a temporal window [tᵥ, tᵥ + tₗₒₒₚ] where interfering transactions can arrive. Since these transactions still arrive following a Poisson process, we know that the probability of no interference (i.e., no interfering transaction arrives in tₗₒₒₚ) is

where Λᵢₙₜ is the TPS for interfering transactions. This factor translates into a probability of a successful sandwich of the form

This is a term that depends on the time needed to process transactions in a loop, which in principle is independent of the block time. In case this tₗₒₒₚ is reduced when reducing slot time, sandwich profitability will always increase by going from 400 ms to 150 ms.

2.4 - Stake-Ordered Propagation and Its Implications

Alpenglow specifies that once a relay receives its assigned shred, it broadcasts its shred to all nodes that still need it, i.e., all nodes except for the leader and itself, in decreasing stake order (cfr. Alpenglow paper page 13). While this design choice appears to optimize latency toward finality, it introduces important asymmetries in how information is disseminated across the network.

From a protocol efficiency standpoint, prioritizing high-stake validators makes sense: these nodes are more likely to be selected as voters, and their early participation accelerates the construction of a supermajority certificate. The faster their votes are collected, the sooner the block can be finalized.

However, this propagation order comes at the expense of smaller validators, which are placed at the tail end of the dissemination process. As a result:

Small validators may receive shreds later, increasing the probability that by the time they vote, a certificate is already formed without their participation.

Given that voting is rewarded, these validators are effectively disadvantaged: they may miss out on reward opportunities not due to faults or downtime, but due to structural delays in propagation.

This introduces a self-reinforcing inequality: high-stake validators receive data earlier, vote earlier, and earn more rewards, thereby compounding their stake and influence over time.

In short, while stake-ordered propagation helps optimize time-to-finality, it imposes a latency tax on small validators, which may undermine long-term decentralization by suppressing their economic participation.

However, it is worth mentioning that, Turbine has more than one layer, meaning that most small stake may get the shreds with multiple network delays. In principle, with Rotor, this stake is only impacted by the transmission delay of the relay.

2.5 - Block Propagation and Slice Failure

Lemma 7 presents a probabilistic bound ensuring that a slice can be reconstructed with high probability, provided a sufficient number of honest relays. While the lemma is mathematically sound, its real-world implications under the chosen parameters raise several concerns.

In particular, the paper adopts a Reed–Solomon configuration with Γ = 64 total shreds and a decoding threshold γ = 32, meaning that any 32 out of 64 shreds are sufficient to reconstruct a slice. Each shred is relayed by a node sampled by stake, and blocks are composed of 64 slices. Finality (via Rotor) requires all slices to be reconstructed, making the system sensitive to even a single slice failure.

The authors justify slice reliability using a Chernoff bound, but for Γ = 64, this is a weak approximation: the Chernoff bound is asymptotic and performs poorly in small-sample regimes. Using an exact binomial model instead, we can estimate failure probabilities more realistically.

Assume 40% of relays are malicious and drop their shreds (pₕₒₙₑₛₜ = 0.6). The probability that fewer than 32 honest shreds are received in a single slice is:

or

This gives P(X < 32) = 0.06714, which represents the single slice failure probability. Since Rotor requires all 64 slices to succeed, the block success probability becomes:

from which the block failure probability is

This is a very high failure probability in the case of a 40% Byzantine stake.

The situation improves only if:

Γ increases (more shreds per slice), or

γ decreases (less redundancy required), or

The system is heavily over-provisioned.

For instance, with Γ = 265 and γ = 132, the slice failure rate under 40% Byzantine stake drops dramatically (though still around 3%), but this imposes higher network and computation costs.

The issue, then, is not the lemma itself, but the practicality of its parameters. While the theoretical bound holds as γ → ∞, in real systems with finite Γ, the choice of redundancy has significant implications:

Higher Γ increases resilience but adds bandwidth and decoding load.

Low Γ, as used in current Solana deployments (e.g., 32 shreds), severely limits robustness without over-provisioning.

2.6 - Message Handling and DDoS Risk

Alpenglow’s messaging system relies on small (<1,500 byte) UDP datagrams for vote transmission (Section 1.4, Page 6). These messages are authenticated using QUIC-UDP or traditional UDP with pairwise message authentication codes (MACs), derived from validator public keys. On receipt, validators apply selective storage rules—only the first notarization vote per block from a given validator is stored (Definition 12, Page 17), with all duplicates ignored.

While this mechanism limits the impact of duplicate votes on consensus itself, it does not eliminate their resource cost. In practice, nodes must still verify every message’s MAC and signature before deciding to store or discard it. This opens a subtle but important attack vector: authenticated DDoS.

A validator controlling less than 20% of the stake can send large volumes of valid-looking, authenticated votes, either well-formed duplicates or intentionally malformed packets. These messages will be processed up to the point of verification, consuming CPU, memory, and network bandwidth on recipient nodes. If enough honest nodes are affected, they may be delayed in submitting their own votes.

This has two possible consequences:

1. Triggering Skip Certificates:

If more than 60% of stake skip votes, even if the leader and most voters were honest. While Alpenglow preserves safety in such cases, liveness is degraded.

2. Selective performance degradation:

Malicious actors could preferentially target smaller or geographically isolated validators, increasing their latency and further marginalizing them from the consensus process.

It’s important to stress that the attack cost is minimal: only the minimum stake required to activate a validator is needed. Indeed, in Alpenglow, votes are not transactions anymore, and SOL does not have the goal of being a spam protection token. Once active, a malicious node with valid keys is authorized to send signed votes, and these must be processed by peers. Unlike traditional DDoS, where filtering unauthenticated traffic is trivial, here the system's correctness depends on accepting and validating messages from all honest-looking peers.

While Alpenglow does not rely on message ordering or delivery guarantees, it remains vulnerable to resource exhaustion via authenticated spam, especially under adversaries who do not need to compromise safety thresholds to cause localized or network-wide disruption.

2.7 - Latency, Processing, and the Stake–Bandwidth

Several aspects of Alpenglow’s evaluation rest on assumptions about network behaviour and validator operations that, while simplifying analysis, may obscure practical challenges in deployment.

2.7.1 - Simplified Latency Assumptions

The simulations in the paper assume a constant network latency, omitting two critical factors that affect real-world performance:

Latency variability: network delays are not constant but fluctuate due to congestion, routing instability, and geographic distance.

Packet loss: especially for UDP-based protocols, loss is non-negligible and may be bursty or asymmetric. This can lead to unreliable shred or vote propagation, particularly under adverse conditions or targeted load.

These effects can meaningfully impact both block propagation and vote arrival times, and should be explicitly modelled in simulations.

2.7.2 - Packet Transmission vs. Processing Delay

Another element that requires a deep dive is the distinction between message reception and message processing. While validators may receive a shred or vote in time, processing it (e.g., decoding, MAC verification, inclusion in the vote pool) introduces a non-trivial delay, especially under high network load.

The absence of empirical measurements for this processing latency, especially under saturated or adversarial conditions, may limit the trustworthiness of the estimated time-to-finality guarantees.

2.7.3 - Stake Does Not Equal Bandwidth

Finally, Section 3.6 (Page 42) assumes that stake is a proxy for bandwidth, that is, validators with more stake are expected to provide proportionally more relay capacity. However, this assumption can be gamed. A single operator could split its stake across multiple physical nodes, gaining a larger share of relaying responsibilities without increasing aggregate bandwidth. This decouples stake from actual network contribution, and may allow adversarial stake holders to degrade performance or increase centralization pressure without being penalized.

2.8 - Implications of PoH Removal

One consequence of removing PoH from the consensus layer is the loss of a built-in mechanism for timestamping transactions. In Solana’s current architecture, PoH provides a cryptographic ordering that allows validators to infer the age of a transaction and deprioritize stale ones. This helps filter transactions likely to fail due to state changes (e.g., nonces, account balances) without incurring full execution cost.

Without PoH, validators must treat all transactions as potentially viable, even if many are clearly outdated or already invalid. This increases the computational burden during block execution, as more cycles are spent on transactions that ultimately revert.

Current on-chain data show that failed bot transactions account for ~40% of all compute units (CUs) used, but only ~7% of total fees paid. In other words, a disproportionate share of system capacity is already consumed by spammy or failing transactions, and removing PoH risks further exacerbating this imbalance by removing the only embedded mechanism for temporal filtering.

While PoH removal simplifies protocol architecture and decouples consensus from timekeeping, it may unintentionally degrade execution efficiency unless new mechanisms are introduced to compensate for the loss of chronological ordering.

3 - Economic Impact and Game Theory

The Alpenglow whitepaper doesn’t provide a full description of how rewards are partitioned among different tasks fulfilled by validators. However, there are features that are less dependent on actual implementation. With this in mind, this section is focussed on describing some properties may arise from the rewarding system.

3.1 - Self reporting of tasks

As described in the paper, during an epoch e, each node counts how many messages (weighted messages, or even bytes) it has sent to every other node and received from every other node. So every node accumulates two vectors with n integer values each. The nodes then report these two vectors to the blockchain during the first half of the next epoch e + 1, and based on these reports, the rewards are being paid. This mechanism mostly applies to Rotor and Repair, since voting can be checked from the signatures in the certificate.

For Repair, while the design includes some cross-validation, since a validator vᵢ sends and receives repair shreds and reports data for other validators vⱼ ≠ vᵢ, there is still room for strategic behaviour. In particular, since packet loss is inherent to UDP-based communication, underreporting repair messages received from other validators cannot easily be flagged as dishonest. As a result, nodes are not properly incentivized to provide accurate reporting of messages received, creating a gap in accountability.

The situation is more pronounced for Rotor rewards, which are entirely based on self-reporting. When a validator vᵢ is selected as a relay, it is responsible for disseminating a shred to all validators (except itself and the leader). However, because there is no enforced acknowledgment mechanism, rewards cannot depend on whether these shreds are actually received by every node, only on whether the slice was successfully reconstructed. In this framework, a rational relay is incentivized to minimize dissemination costs by sending shreds only to a subset of high-stake validators, sufficient to ensure that γ shreds are available for decoding. This strategy reduces bandwidth and CPU usage while preserving the probability of slice success, effectively allowing relays to free-ride while still claiming full credit in their self-reports.

3.2 - No stake, no bandwidth

As discussed in Sec. 2.7.3, a node operator can reduce hardware costs by splitting the stake across multiple identities, exploiting the fact that expected bandwidth delivery obligations are proportional to stake. This allows the operator to distribute the load more flexibly while maintaining aggregate influence.

Alpenglow paper, in Sec. 3.6, introduces a mechanism that penalizes validators with poor performance. Precisely, the selection weight of these validators is gradually reduced, diminishing their likelihood of being chosen to do tasks in future epochs. While this mechanism intends to enforce accountability, it also creates a new incentive to underreport. Since selection probability affects expected rewards, validators now have a strategic reason to downplay the observed performance of peers.

In this context, underreporting becomes a rational deviation: by selectively deflating the recorded bandwidth contribution of others, a validator can increase the relative selection weight of its own stake. This dynamic may further erode the trust assumption behind self- and peer reporting, and eventually amplify the economic asymmetry between high- and low-resource participants.

3.3 - Strategic Vote Withholding

Although Alpenglow removes explicit vote transactions, its reward mechanism still admits a form of time-variability compensation gameability. Specifically, there exists a potential vulnerability in which a validator can strategically delay its vote to maximize the likelihood of earning the special reward for broadcasting the first Fast-Finalization Certificate (FFC).

To incentivize timely participation, Alpenglow rewards validators for voting and relaying data, with additional bonuses for being the first to submit certificates. This mechanism, while well-intentioned, opens the door to timing-based exploitation.

Consider a validator v controlling X% of the total stake, where X is large enough to push cumulative notarization votes past the 80% threshold. During the first round of voting for a block b in slot s, validator v monitors the notarization votes received in its Pool. The strategy works as follows:

Vote Withholding: Validator v refrains from casting its NotarVote until it observes that the cumulative stake of received votes exceeds (80 − X)% but remains just under 80%. This ensures the FFC has not yet been triggered.

Timed Vote Submission: We are at time t = t₀ + δₑₛₜ + ε, where t₀ is the slot start time, δₑₛₜ is the estimated network propagation delay for 80% of the stake, and ε is a small buffer. The validator v submits a NotarVote. To cover fallback finalization, v may also submit a NotarFallback vote.

Fast-Finalization Certificate Issuance: Upon submitting its vote, the total voting weight reaches or exceeds 80% (by construction). Validator v immediately generates an FFC and broadcasts it. By exploiting a low-latency network position, v increases the likelihood that its certificate is the first observed, thereby capturing the special reward.

Fallback to Slow Path (if needed): If v’s FFC is not the one finalized, then its original NotarVote still contributes to the slow path. This yields a standard voting reward, though the special bonus is forfeited.

This strategy has asymmetric risk: the validator either receives the normal reward (if it fails) or both the normal and special reward (if it succeeds), with no penalty for delayed voting. As such, validators with low-latency infrastructure and accurate network estimation have an economic incentive to engage in this behaviour, reinforcing centralization tendencies and undermining the fairness of the reward distribution.

3.4 - Impact of Randomness on Rewards

In this section, we examine how inherent randomness in task assignment affects validator rewards. Even if a validator fulfils every duty it’s assigned (voting, relaying, repairing), the Alpenglow protocol still injects non-determinism into its reward streams. Voting remains predictable, since every validator casts a vote each slot, but relay income depends on the stochastic selection of one of Γ relays per slot, and repair income depends both on being chosen to repair and on the random need for repairs. We use a Monte Carlo framework to isolate and quantify how much variance in annual yield arises purely from these random sampling effects.

In our first simulation suite, we fix a validator’s stake share and vary only the split between voting and relay rewards, omitting repair rewards for now to isolate their effects later. Concretely, we let

for each (f_relay, f_vote) pair, and for each epoch in the simulated year, we:

Compute the issuance: Determine the epoch’s inflation payout from a 4.6% annual rate, decaying 15% per year down to a 1.5% floor.

Set per-task rewards: We compute the reward per vote and the reward per relay task.

Sample relay assignments: Draw the number of times our validator is selected as one of Γ = 64 relays in each epoch’s 18,000 slots.

Accumulate rewards: We compute the rewards accrued.

Compound over epochs: Roll rewards into stake each epoch to compute the year-end APY.

First simulations assume a stake share of 0.2% and a network-wide stake rate of 65%. This framework lets us see how different reward splits affect the dispersion of APY when relay selection is the sole source of randomness.

The plot above shows the Probability Density Function (PDF) of APY obtained by varying the Relay rewards share. We can see that up to a 50% split, the variance is not dominating the rewards, where the APY is approximately 6.75% from the 5th percentile (p05) to the 95th percentile (p95).

If we reduce the stake share to 0.02% (with current stake distribution, this corresponds to the 480th position in validator rank - 93.5% cumulative stake) we see that 50% share has some variability that may affects rewards. In this scenario, APY varies from 6.74% for p05 to 6.75% for p95. Even though a 0.01 percentage-point spread seems negligible, over time and combined with other asymmetries, it can create meaningful divergence in rewards.

Accordingly, we adopt a 20% relay‐reward share for all subsequent simulations. Indeed, we can see that, by fixing the relay‐reward share at 20%, the spread in APY distribution is mostly negligible moving from 0.02% stake share to 2%.

With repair rewards added, we now set

We also assume that 5% of slots on average require a repair fetch.

Running the same Monte Carlo simulations under these parameters reveals two key effects:

Increased asymmetry for low-stake validators: Unlike voting (deterministic) and relaying (high-frequency sampling), repair rewards are both infrequent (only 5% probability a slot is not in Blockstore) and random in assignment. A small validator may be selected for very few repair tasks, or none at all, over the course of a year. As a result, their share of the 5% repair-reward pot can vary wildly, even if their stake share remains constant.

Wider APY dispersion: When we plot APY versus stake share, the repair component introduces a pronounced “tail” in the distribution for lower-stake nodes. Whereas previously the 5th–95th percentile band was on the order of 0.01 pp for small stakes, adding repair rewards can expand that spread by 0.04 pp, enough to materially affect ROI comparisons and reinforce centralization pressures.