Chorus One is now a part of Bitwise. Bitwise is a global, crypto-first asset manager with $11 billion+ in client assets and a diverse suite of investment solutions. Learn more about how Chorus One is growing as a part of Bitwise at onchain.bitwiseinvestments.com.

Oops! Something went wrong while submitting the form.

Fill in the form below to download the report

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Fill in the form below to download the report

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Fill in the form below to download the report

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Crypto Research You Can Trust

The crypto space is evolving rapidly and can get daunting for investors. That is why we have a dedicated team of researchers who turn the complex technical advancements in the field into easily understandable research reports. These reports are highly valued by institutions and investors who want to stay up-to-date with the latest developments in the crypto world.

The State of Schedulers on Solana

Streaming, Batching, and the Economics of Execution Timing

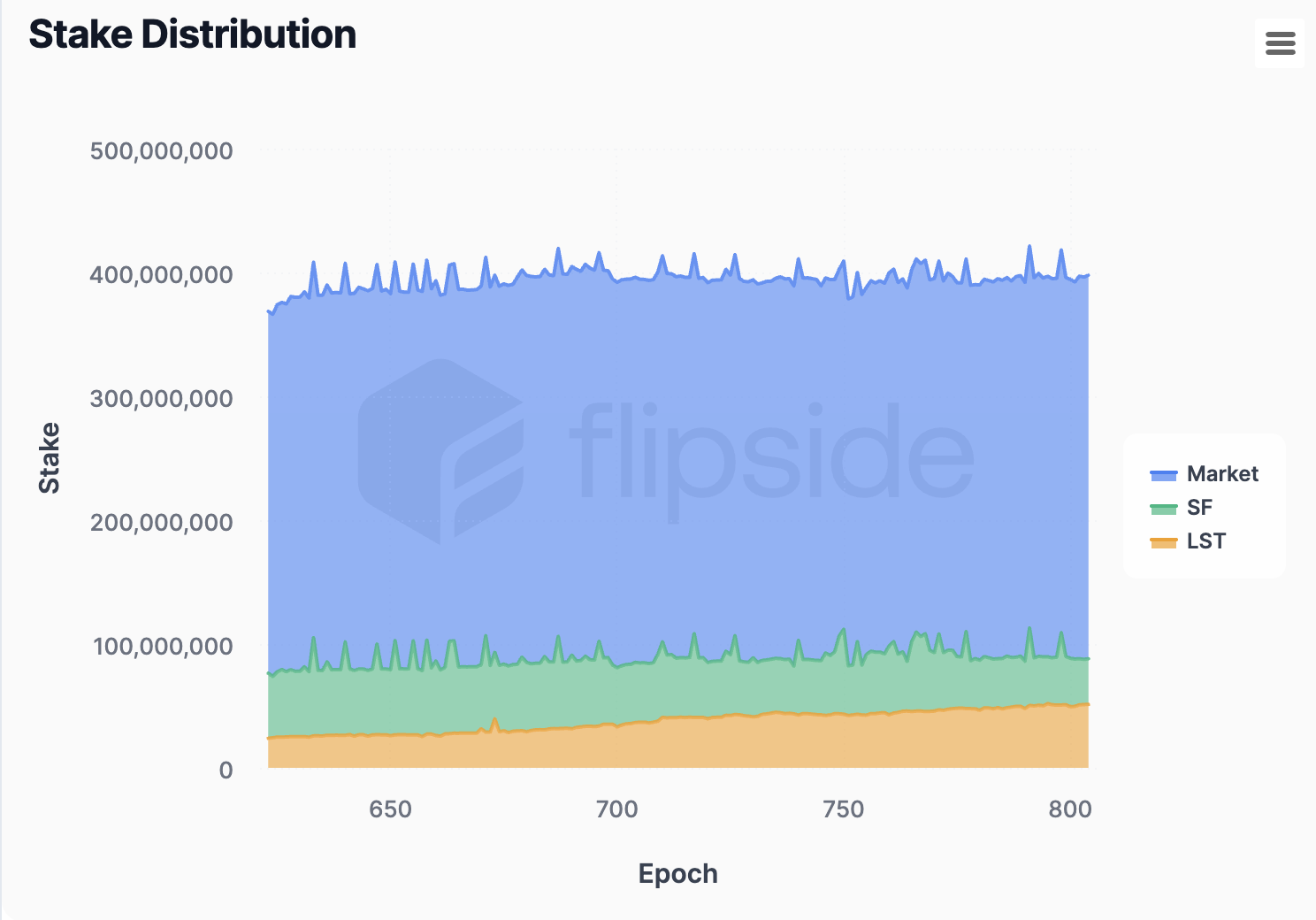

About 65% of SOL is staked, with the Solana Foundation Delegation Program (SFDP) still playing a significant role, although its share in total stake has fallen below 10%.

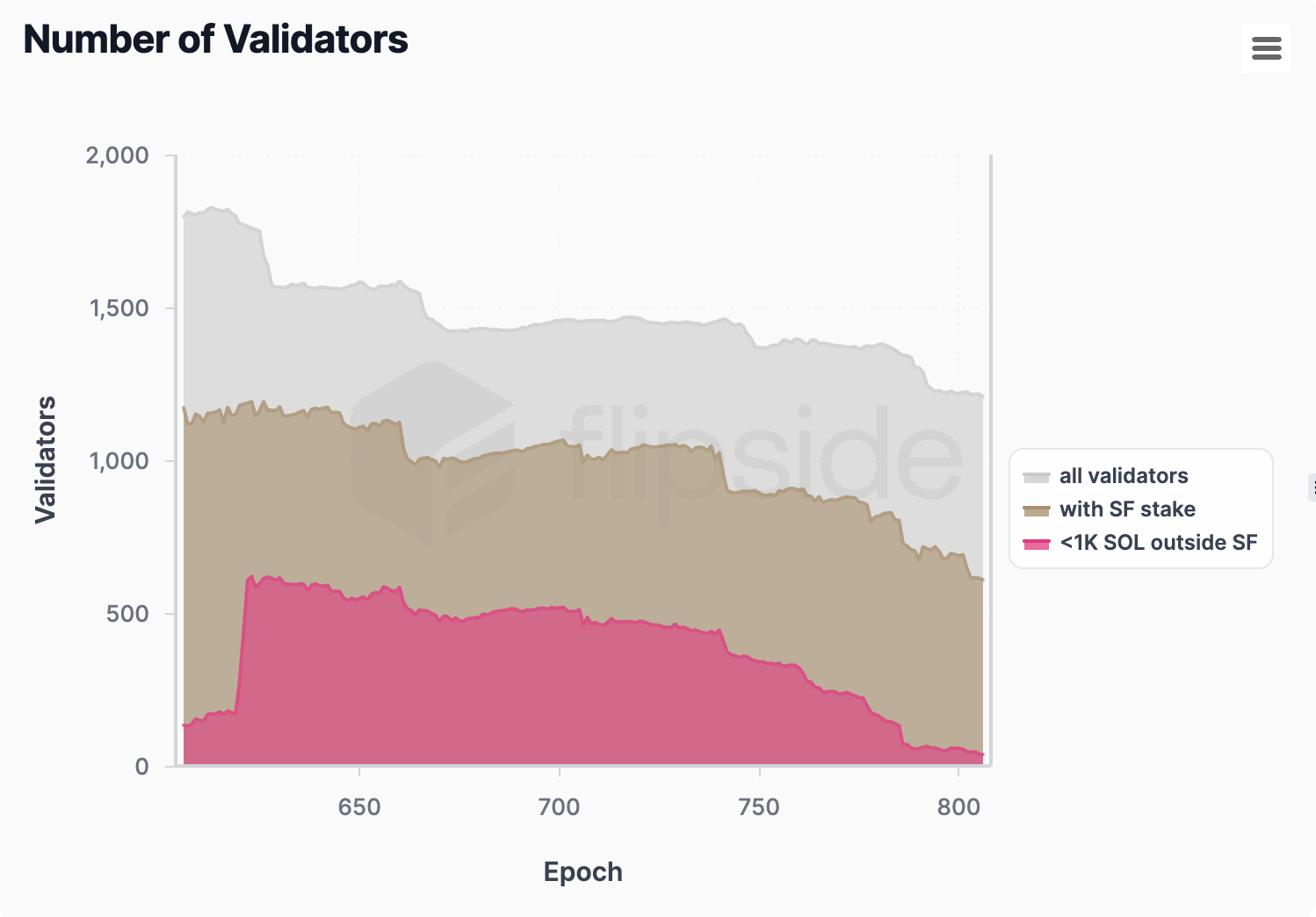

The number of active validators has dropped to 1,216, with SFDP now supporting 616 of them—half of the total, down from over 1,100.

The SFDP has become more selective, focusing support on validators that have been active in the Solana community and actively seek outside stake.

Liquid staking tokens (LSTs), such as JitoSOL, have gained influence, often being delegated to validators in the SFDP, and now represent 26% of the total stake of SFDP validators.

SFDP and LSTs are essential for maintaining network decentralization due to the geographical constraints they place on validators.

Only 48% of SFDP validators are profitable under current conditions; without SFDP support, that number drops to 32%.

Removing voting costs significantly boosts profitability—profitable validators increase by 50%, and the minimum stake required for profitability drops by 68%.

This increase in profitability should become noticeable after the implementation of Alpenglow.

Introduction

Solana has one of the highest staking rates among all blockchains. As of now, 65% of the circulating SOL is staked, which is significantly higher compared to ETH’s 29%. Several factors contribute to this difference, including the attractive yields ranging from 8% to 12% that Solana provides, as well as a positive outlook for SOL’s performance among its holders. However, another important factor is the Solana Foundation Delegation Program (SFDP), which accounts for a significant portion of the staked SOL.

Helius wrote a comprehensive and detailed piece about the Program, but almost a year has passed since its publication, making it a good time to revisit the subject. In this article, we will examine the current state of the program to understand its effect on Solana’s validator landscape and what the network might look like if the SFDP were to end.

Solana Staking Market Segmentation

The Solana staking market can be categorized into three distinct segments:

Market Stake: SOL staked natively.

Liquid Staking Tokens (LSTs): Stake delegated through staking pools.

As of epoch 804, the total amount of staked SOL is 397 million, with the general market delegating 309 million, the Solana Foundation 37 million, and LSTs contributing 51 million. Over time, we have seen steady growth in LST stake and a decrease in SF delegations, which now make up slightly less than 10% of the total stake.

Solana stake is managed by a total of 1,216 ****validators, down from a peak of 1,800. The number of validators receiving delegations from SFDP has decreased from over 1,100 to 616, which still makes up 50% of the entire validator set, representing a significant decrease from the initial 72%. We also observe the validators with less than 1K SOL delegated outside of SF—currently at 46, down from over 600.

The 1K SOL threshold is important because SF decided to stop supporting validators that receive a Foundation delegation for more than 18 months and are not able to attract more than 1K SOL in external stake.

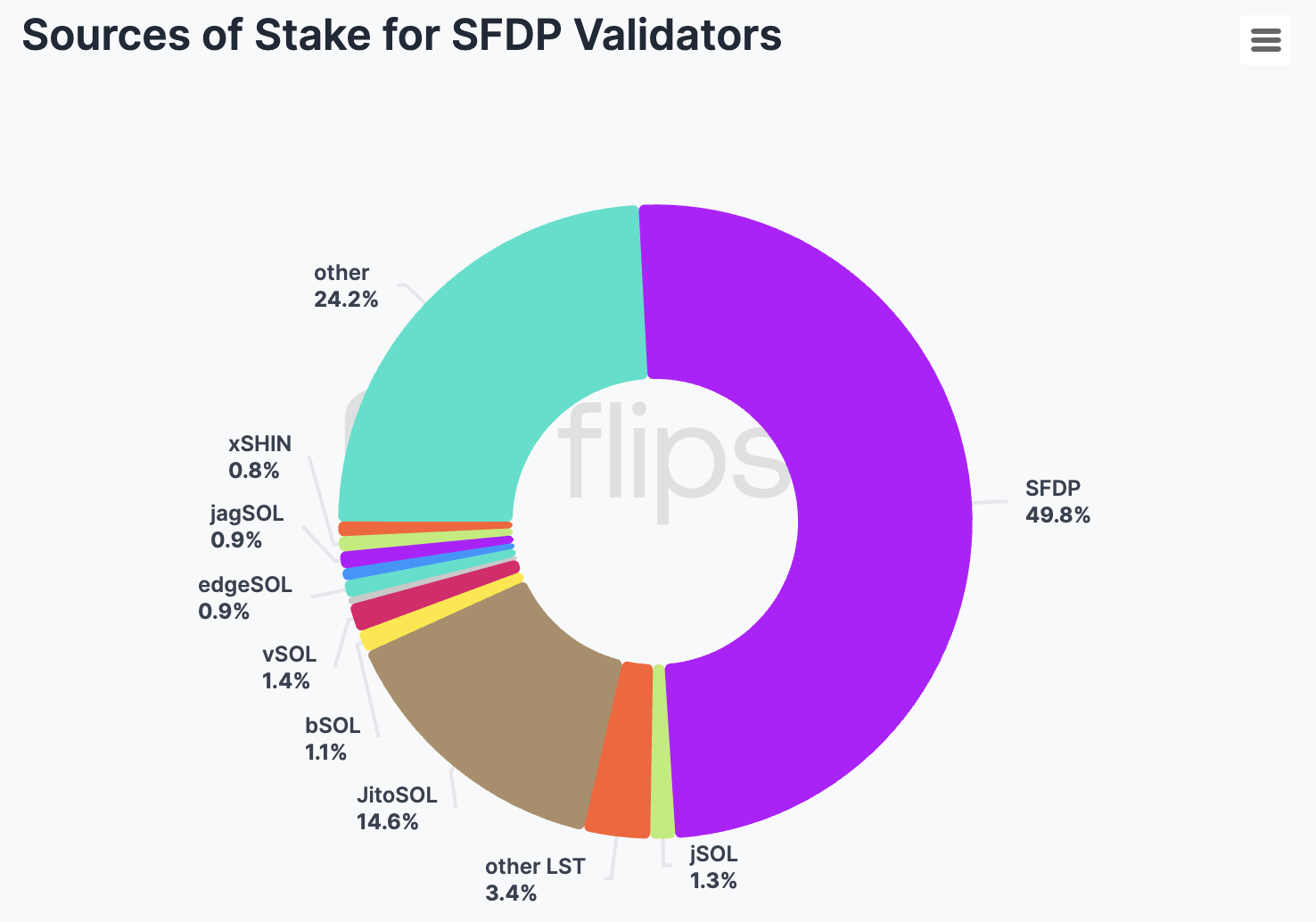

Delegations from the Program make up 49.8% of the total stake delegated to validators participating in SFDP. This is significant, but it also shows that over half of the stake comes from other sources, which is a positive sign.

Another opportunity (or lifeline) for smaller validators is provided by LST staking pools, which collectively make up 26% of the stake delegated to validators participating in the SFDP. Notably, the Jito stake pool, represented by the JitoSOL token, has accumulated 17.8 million SOL out of a total of 397 million SOL currently staked. Due to this substantial amount, being one of the 200 validators receiving delegation from the pool is highly rewarding, currently by around 89K SOL. Of the 17 million native SOL in the Jito pool, nearly 11 million, or 65%, ****are delegated to SFDP participants.

For Blaze (bSOL), another popular staking pool, 0.8 million of the 1.1 million SOL, accounting for 72%, is delegated to SFDP participants. For JPOOL (jSOL), it’s 83%, and for edgeSOL, it’s as high as 87%. Many of the LST pools highly depend on outstanding voting performance, resulting in a cut-throat competition between validators to receive delegation. The validators often run backfilling mods to increase the vote effectiveness and receive stake. Chorus One has analyzed these client modifications in a separate article.

We also observe that the SFDP and LSTs are vital for maintaining Solana's decentralization. This results from the geographical restrictions imposed by the Foundation and staking pools on validators.

When examining the total stake of validators participating in SFDP, only 31 had accumulated more than 300K SOL, while 249 had less than 50K SOL delegated.

Looking at the top 20 validators individually, the validator with the highest stake, Sanctum, accumulated a total of 850K SOL in delegations. In contrast, the 20th validator's total stake drops to 351K SOL. The size of the SFDP delegation doesn’t exceed 120K SOL in this group.

In the remaining group of 589 validators, the median total stake is 65K SOL, and the median SF delegation is 40K SOL, indicating that many validators rely heavily on the Foundation for their operations.

Validator Profitability

The node operating business has become very competitive in recent years. This is especially true on Solana, where validators often run modified clients or lower their commissions to unhealthy levels to gain an advantage. And like any other business, you can't stay unprofitable for too long.

And what does too long mean on Solana? To answer this question, we group validators into cohorts. We group time into periods of 10 epochs: every 10 epochs, a new period starts. Every period, a new cohort of validators emerges. We can follow these cohorts and see how the composition of the validator set changes over time, and in which period the validators started. For this analysis, we only consider validators with at least 20k SOL at stake.

Source: Chorus One Internal

Based on the first graph, the survival rate for most cohorts falls below 50% after approximately 200 to 250 epochs. Similarly, the second graph shows that validators who started around epoch 550 see the steepest drop in survival rates. This suggests that the too long in terms of unprofitability on Solana means around 250 epochs.

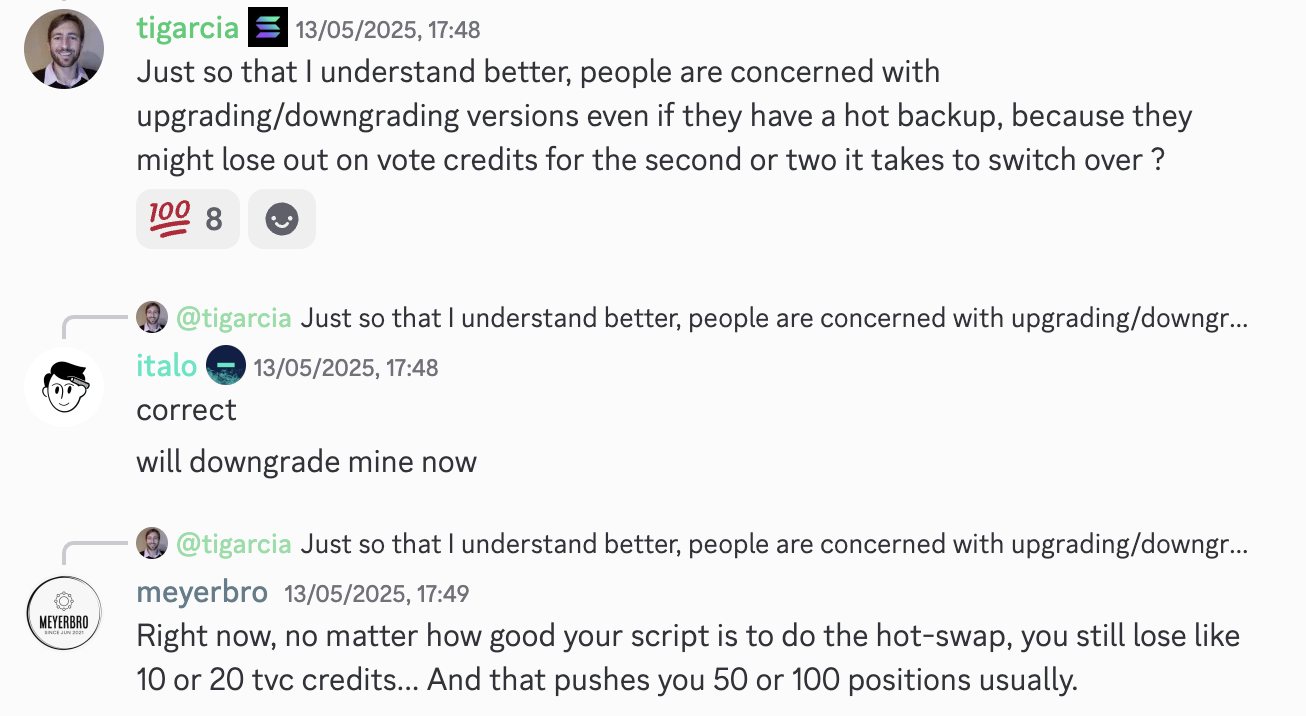

One indicator of how fiercely competitive the smaller validator market has become is the scramble to join the JitoSOL set, where validators hesitate to upgrade the Agave client because they risk losing several vote credits during the update. Any loss of vote credits is problematic since Jito updates the validator pool only once every fifteen epochs. Additionally, being outside the set decreases a validator’s matching stake from SFDP. Therefore, with the current 89K SOL Jito delegation goal, a validator could lose 178K stake if something goes wrong during the update.

Sources that are not easily traceable on the chain, such as selling swQoS or selling transaction order flow for back-running.

Of the three on-chain traceable revenue sources, MEV and block rewards are highly dependent on network activity. In contrast, inflation rewards are a function of the Solana inflation schedule and the ratio of staked SOL.

Validator performance also impacts yields. Opportunities to increase inflation rewards are limited, as almost all validators receive close to the maximum vote credits possible. Some validators overperform in voting, but APY gains from it are close to a rounding error—0.01%. Currently, the inflation rewards produce the highest gross (before commission) returns of around 7.3% annually, when compounded. The most effective voting optimizations include mods that enable vote backfiling. This opportunity, however, could be short-lived as intermediate vote credits update rolls out in the coming months. That is, unless the update is entirely abandoned because of the introduction of Alpenglow.

MEV tips and block rewards see higher upside from optimizations. Based on current activity (June 2025), tips yield between 0.75% and 0.9% in annualized gross APY, while block rewards yield between 0.55% and 0.65%. Both have a luck factor in it—if there’s a particularly juicy opportunity, e.g., for arbitrage, the searchers will be willing to pay more to extract it. Thus, the bigger the stake the validator has, the higher the chance it will receive outsized tips or block rewards. The validator optimizations for MEV tips and block rewards involve updates to the transactions ingress process or the scheduler.

In absolute terms, all revenue sources depend on the stake a validator has.

Costs

Solana is infamous for its high-spec hardware requirements and the overall costs it imposes on validators running the nodes. These costs include:

Hardware, including a backup node, network bandwidth, and monitoring software: Solana requires running on bare metal machines for it to make economic sense. Multiple providers offer servers in data centers worldwide, with some offering Solana-specific options. The annual cost of a high-performance node is approximately $20,000. A backup node with lower specs could be half the cost, at around $10,000. The top-of-the-shelf sets can go for even $45,000.

Voting costs: Solana validators achieve consensus by voting in each slot. There are 432,000 slots in an epoch, which currently lasts around two days. Each vote is a transaction, which costs a base fee of 5000 lamports, or 0.000005 SOL. If a validator were to vote in every slot, the cost of voting per epoch would be 2.16 SOL. Since this is not what happens in practice, a more accurate estimate is 2 SOL per epoch, or 1 SOL per day in voting costs. At current SOL prices, validators must give away approximately $60,000.

The total cost of running the Solana node, excluding any people costs, in June 2025 ranges from $90,000 to $105,000.

Profitability Estimation

To establish the profitability of a validator participating in an SFDP, we will:

On the revenue side:

Compute the APY of Chorus One over the last month. This APY will serve as an indicator of network activity.

Take the inflation commission and MEV commission data for each participating validator.

Compute the annualized revenue by multiplying the stake, Chorus One APY, and validators' commissions.

Based on the average SOL/USD price for the month ($161), compute the revenue in USD.

On the costs side:

Assume the fixed hardware costs of USD 30,000 per year.

Assume voting costs of 1 SOL per day.

Based on the average SOL/USD price for the month, compute the costs in USD.

With the above assumptions, we measure the profitability of validators participating in SFDP considering their: (1) total active stake; (2) only outside stake, without SF delegation; (3) only outside stake, but assuming no voting costs.

If the current market conditions and network activity remain unchanged for the entire year, in the first group**,** 295 SFDP validators would be profitable (48%), with a median profit of $134,283. Conversely, 319 validators are facing a median loss of -$51,473.

It is important to note that the graphs in this section are capped at $700,000 on the y-axis for clarity; however, some validators have profits that exceed this amount.

However, the stake received from the Foundation is not evenly distributed among all validators. The average stake delegated from the Program to profitable validators is 94,366 SOL, while to unprofitable ones, it is only 26,969 SOL.

The last profitable validator holds a stake of 33,242 SOL from SFDP and 21,141 SOL from outside sources, which enables it to earn $1,710.

There is a noticeable difference in commissions between the profitable and unprofitable groups: the profitable validators have an average inflation commission of 1.92%, compared to 1.51% in the unprofitable group. Similarly, the average MEV commission in the profitable group is 7.36%, compared to 5.44% in the unprofitable group.

Source

Things get less rosy if we consider only the outside stake, without the SFDP delegation. The number of profitable validators decreases to 200, which accounts for 32% of the total, with a median profit of $35,692. The number of unprofitable validators increases to 414, with a median loss of $78,912.

The last profitable validator has 95,030 SOL in outside stake (although, with 0% inflation and MEV commissions) and earns $126.31. The minimum outside stake guaranteeing profitability is 56,618 SOL, with commissions at 5% inflation and 10% MEV. This is enough to get $5,441.52.

Among the profitable validators, the average inflation commission is 1.75%, while the average MEV commission is 7.57%. For the unprofitable nodes, the commissions decrease to 1.7% and 5.8%, respectively.

It is well known that voting costs impact validators the most. With the SOL price at $161 (as used in this analysis), validators spend around $59,063 on voting only. For this reason, node operators have long advocated for the reduction or complete removal of voting fees. This wish will be finally fulfilled with Alpenglow, Solana’s new consensus mechanism announced by Anza at Solana Accelerate in May 2025. It is ambitiously estimated that the new consensus will replace TowerBFT in early next year.

We analyze the scenario in which voting doesn’t generate costs. Even if we only consider the outside stake, it makes a big difference.

The number of profitable validators increases by 50%, from 200 to 303, compared to the second scenario. The median profit in this group reaches $74,328. While there are still 311 unprofitable validators, the median loss falls to $23,576.

The minimum stake required to guarantee profitability is 17,988 SOL, representing a 68% decrease compared to the scenario that includes voting costs.

Still, the difference in average commissions is impactful—1.92% on inflation and 7.29% on MEV in the profitable group compared to 1.51% and 5.47% in the unprofitable one.

Conclusions

The SFDP continues to play a vital role in the Solana ecosystem. Recently, the Foundation has shifted its focus to support validators who make meaningful contributions to the Solana community and actively pursue stake from external sources, aiming to create a more engaged and sustainable validator network.

With a more selective approach from the Foundation, LSTs come as a crucial source of stake for smaller validators. SOL holders like them, which is evident in their constantly increasing stake; however, the competition to get into the set is prohibitively tough. Still, the importance of SFDP’s stake matching mechanism cannot be understated in light of delegations from LSTs.

Together with LSTs, the SFDP stake makes up 22% (88 million SOL) of the total SOL staked. Since both impose geographical restrictions on validators, they are crucial to keep Solana decentralized in an era where even negligible latency improvements from co-location are exploited.

Currently, many validators remain unprofitable, even with support from SFDP. Commission sizes play a role here—setting them too low doesn’t seem to help with getting enough stake to run the validator profitably.

Another force negatively impacting the validators’ bottom line is voting cost. When network activity and SOL price are high, this is the time when validators should offset the periods with little action. Unfortunately, due to the voting process, a significant portion of revenue is lost. The solution, Alpenglow, is on the horizon, and it cannot come fast enough to reduce pressure on validators. Eliminating the voting costs should enable the Solana Foundation to step away further and let the network develop on the market’s terms, without excessive subsidy.

The Berachain ecosystem is about to transform significantly with the upcoming Bectra upgrade, which introduces multiple critical EIPs adapted to Berachain’s unique architecture. Perhaps, the most revolutionary EIP is EIP-7702, which enables regular addresses to adopt programmable functionality.

This major milestone also introduces a game-changing feature BERA stakers have been waiting for: the ability to unstake their tokens from validators. Until now, once BERA was staked with a validator, it remained indefinitely locked. Bectra changes this fundamental dynamic, bringing new flexibility to the Berachain staking landscape.

Bectra is the Berachain version of Pectra, the latest Ethereum hard fork that introduced significant improvements to validator flexibility and execution layer functionality. For those interested in a deeper technical analysis of the upgrade, we recommend reading Chorus One’s comprehensive breakdown on Pectra: The Pectra Upgrade: The Next Evolution of Ethereum Staking.

Practical Changes

Although the biggest Bectra change might be EIP-7702 (account abstraction), the biggest change for Berachain that is different from Pectra is the ability for BERA stakers to withdraw their staked assets from validators. This fundamentally alters the validator-staker relationship, as validators must now continuously earn their delegations through performance and service quality.

How Unstaking Works

As a user who has staked BERA with a validator, it's important to understand that you don't directly control the unstaking process. Here's what you need to know:

Contact Your Validator: If you want to unstake your BERA, you'll need to contact the validator you staked so they can put you in touch with the Withdrawal Address Owner in order to request a withdrawal.

Validator Controls the Process: Only the validator (or the entity controlling the validator's Withdrawal Credential Address) can initiate the unstaking process.

Withdrawal Fee: Be aware that every withdrawal requires a fee, which the validator may pass on to stakers or absorb as part of their service offering.

Waiting Period: After your validator initiates your withdrawal, there's approximately a 27-hour (256 epochs) waiting period before the tokens become available.

Receiving Your Tokens: The unstaked BERA will be returned to the validator's Withdrawal Credential Address, not directly to you. The Withdrawal Address Owner will need to transfer your tokens to you in a separate transaction.

Important Considerations:

Trust Relationship: The unstaking process highlights the importance of staking with trusted validators who have clear policies for handling withdrawal requests.

No Direct Control: As a regular user, you cannot directly unstake your BERA from the protocol; you must work through your validator.

Potential Delays: Your unstaking timeline depends on how quickly your validator processes your request (in most cases, it would depend on the Foundation or a custodian), in addition to the protocol's 27-hour waiting period.

Minimum Stake Requirements: Validators must maintain at least 250,000 BERA staked. If many users request withdrawals at once, the validator might need to process them in batches to maintain this minimum. If a validator's stake falls below 250,000 BERA, they will be removed from the active validator set and will no longer be able to produce blocks or earn rewards. This means they would cease to function as a validator until they stake the minimum amount again.

Redelegation Process

There is currently no direct "redelegation" mechanism in the protocol. If you want to move your stake from one validator to another:

You must first request your current validator to unstake your BERA

Wait for the validator to process your request and for the unstaking period to complete

Once you receive your BERA tokens, you can stake them with a different validator

During this process, you won't earn staking rewards while your tokens are in the unstaking phase.

Staking Process

The staking process itself remains unchanged with the Bectra upgrade. Users can still stake their BERA with any validator, and the validator continues to receive all rewards at their Withdrawal Credential Address.

If there are multiple stakers delegating to a single validator, the protocol does not automatically distribute rewards to individual stakers; this must be handled through off-chain agreements with the validator or through third-party liquid staking solutions.

Implications for BERA Stakers

The introduction of validator stake withdrawals transforms the staking landscape on Berachain in several important ways:

New Staking Dynamics

For BERA stakers, the ability to unstake creates:

Freedom of movement: Switch validators freely without being tied to your original decision.

Strategic control: Adjust your delegation based on performance, risk tolerance or evolving network conditions.

Lower opportunity cost: You can now reallocate your capital when attractive opportunities arise elsewhere.

Competitive Validator Landscape

This new mobility creates a more competitive environment where:

Validators must continuously demonstrate value to retain delegations

Performance metrics like USD value per BGT emitted, PoL ARR and commission rates become critical differentiators

Poor-performing validators (lower BERA staking ARR) face stake migration to competitors

This competitive pressure should drive validators to optimize operations, potentially leading to better returns for stakers and improved network performance.

New Responsibilities With greater flexibility comes increased responsibility:

Active monitoring of validator performance in terms of BERA staking ARR becomes necessary

Ongoing research replaces one-time validator selection decisions

Understanding the trade-offs between staying with a single validator versus frequently moving your BERA to seek better returns.

Knowledge of unstaking mechanisms and timeframes

This creates an opportunity for stakers to be more strategic with their decisions and potentially increase returns by selecting the best-performing validators.

Why Stake with Chorus One

As the Bectra upgrade introduces more competition among validators, choosing the right validator becomes increasingly important. Chorus One stands out as a premier choice for several compelling reasons:

Industry-Leading ARR

Chorus One consistently delivers some of the highest ARRs in the Berachain ecosystem thanks to Beraboost, our built-in algorithm that directs BGT emissions to the highest-yielding Reward Vaults, maximizing returns for our stakers.

Currently, our achieved ARR for BERA stakers has ranged between 4.30% and 6.70%, with longer staking durations yielding higher returns due to compounding effects. For comparison, most BERA LSTs offer an ARR between 4.5% and 4.7%. Our ARR pick up is achieved via our proprietary algorithm (ie, BeraBoost) as well as with active DeFi, also capturing part of the inflation going to ecosystem participants:

Additionally, in terms of incentives captured per BGT emitted (a key metric reflecting a validator’s revenue efficiency), our validator consistently outperforms the average by $0.5 to $1:

Unmatched Reliability and Experience

As a world-leading staking provider and node operator since 2018, Chorus One brings extensive experience to Berachain validation. Our infrastructure features:

Maximum uptime and performance

Redundant systems and 24/7 monitoring

Battle-tested experience across multiple proof-of-stake networks

Transparent Operations & Dedicated Support

We believe in complete transparency with our stakers, with publicly available performance metrics and regular operational updates. Our team is always available to assist with any questions about staking with Chorus One.

Conclusion

The Bectra upgrade represents a significant evolution for Berachain, giving stakers the freedom to unstake and move their BERA between validators. This new flexibility creates both opportunities and responsibilities, as stakers can now be more strategic with their delegations.

In this more competitive landscape, Chorus One stands ready to earn your delegation through superior performance, reliability, and service. Our commitment to maximizing returns for our stakers, combined with our extensive experience, makes us an ideal partner for your BERA staking journey.

Stake with Chorus One today and experience the difference that professional validation can make for your BERA holdings.

This article provides an accessible first perspective on validator timing games on Monad. Practically speaking, validators may intentionally build and gossip their block as late as possible to capture additional value from the incrementally larger set of transactions accruing over slot time.

While timing games have been practiced for multiple years on Ethereum, Monad’s performance-first architecture introduces additional risk considerations. The article recaps timing games, outlines Monad’s architecture, including a recent overhaul of MonadBFT consensus, and describes how sophisticated validators may approach timing games on Monad.

Timing Games & Why They Work

We can loosely define a decentralized network as a set of geographically distributed nodes. More rigorously, we can approximate such a network by its (stake-weighted) network graph, which has a center from which the expected latency to the set of nodes is minimized. As not all nodes are equally close to this center, the network must allow appropriate latency leeway to allow distant nodes to participate - this is a design choice.

In practice, a fast blockchain can be built by co-locating all nodes, but such a structure comes with resiliency trade-offs (e.g. the datacenter shuts down). A more resilient, decentralized architecture like Monad must allow sufficient consensus time for a node that is e.g. located in New Zealand to participate.

Competitive validators may take advantage of this latency leeway to improve the expected value of their blocks by performing two successive actions. First, they minimize their latency to peers, and second, they artificially delay their block proposal. This is referred to as a “timing game”.

To understand why this is profitable, note that as the slot progresses, users keep sending transactions, and therefore, the proposer has a larger amount of transactions to select the final block from. A more nuanced reason is that as the slot progresses, traders have access to more information, and in the case of arbitrage between the chain and another venue (e.g. the most liquid CEX), the expected opportunity value increases as the square root of block time, over time.

Timing games exist on a risk reward curve - the longer the validator delays, the higher the risk of an unwanted timeout resulting in a zero- or negative- payoff. For this reason, an informed validator must quantify the payoff of each unit of delay versus the marginal risk it runs. In summary, a sophisticated approach to timing games hinges on a strong understanding of the network’s topology and transaction arrival dynamics (i.e. the block value over slot time).

Parallelization, Gossiping, and Reorgs in MonadBFT

Monad's consensus mechanism is an improved version of HotStuff called "MonadBFT." HotStuff is a leader-based Byzantine fault-tolerant consensus protocol designed for high throughput and low latency. We will first examine parallelization, before describing how blocks are gossiped to the network.

In MonadBFT, the leader for a slot executes the transactions of the preceding slot **while composing the list of transactions it will include in its block, which will then be executed by the upcoming leader. Intuitively speaking, this means that during its slot, a validator fulfills two tasks: it simulates and settles the transactions passed to it by the validator preceding it in an optimized manner (execution), and packs a block to pass to the validator succeeding it (consensus).

An implication is that any transaction with a state dependency does not yield an execution guarantee until settlement time, which takes place one slot after the transaction has been included. For a typical user, this will not usually be noticeable. For traders competing for limited opportunities, the main implication is a less informed priority gas auction, and if carrying inventory risk (e.g. arbitrageurs), an additional risk margin applied over the other leg(s) of the trade.

Once a validator has decided on its block*,* it sends it out alongside either a quorum certificate (QC), or a timeout certificate (TC) for the previous block. Specifically, a QC attests that the validator has built on the preceding block n, and that this block has been attested to as valid by 2/3 of the network (i.e. an aggregated signature). Conversely, a TC attests that the preceding validator has missed its slot and that the validator has built on the preceding block n-1; a valid TC must also be signed by 2/3 of the network.

The latest iteration of MonadBFT couples any timeout vote with a quorum vote for the most recent block a validator has attested to, which means that any validator which garners a supermajority of votes eventually finalizes. This stands in contrast to previous versions, where a successful timeout quorum would have resulted in a reorg of the validator that had preceded the timed out leader (”tail fork”).

Timing Games on Monad

Timing games on Monad are a race between the QC (validators vote on a block) and TC (validators vote on a timeout) paths. The QC path is faster, with linear overhead (one message per peer), while the TC path is slower, validators must multicast timeout votes and aggregate these into a TC (quadratic overhead).

"Linear overhead" refers to communication complexity that grows proportionally with network size - one leader sending a single message to each of N validators. "Quadratic overhead" occurs when each validator must communicate with many others, causing message volume to grow with the square of the network size as validators both send and receive messages from their peers.

A validator playing timing games must ensure its block reaches a supermajority of the network before a timeout vote does, and therefore, there is a strong incentive to optimize connectivity with the closest 2/3 of peers plus a risk margin for latency or timeouts. Put another way, validators in distant locations might timeout more frequently due to slower block receipt, issuing TCs even as QCs form elsewhere. The upshot is an increased incentive to centralize as timing games spread.

The extent to which a proposer may risk a timeout depends on the marginal value of any delay. This is an empirical question, as traders will time their transactions such that they are late but still run a high inclusion chance (i.e. model the network), whereas retail transaction arrival times can be thought of as unpredictable. An aspect that can be stated is that due to Monad’s shorter block times, the expected value of cross-venue arbitrage is significantly lower than on e.g. Ethereum.

A validator playing timing games benefits from capturing transactions that would have otherwise accrued to a later slot; if all validators play timing games, this results in a competitive outcome with an increased risk profile. Economic incentives are likely to encourage competitive validators to engage in timing games in any scenario, as a decentralized network must accommodate distant participants, and therefore, a delay margin is available for well-networked nodes.

Under previous version of the MonadBFT design, an elevated timeout risk reflected as an increased risk of reorgs. This would have reduced block value upfront, as traders holding inventory risk (e.g. arbitrageurs) adjust their risk margin over the compound risk of not executing due to pipelined consensus plus the reorg risk. In this context, a validator playing timing games on Monad would have reduced the value of the preceding proposer as well.

This is not the case anymore under the current iteration, as timeout votes now carry a quorum vote for the latest block a validator has attested to. This additional information must be gossiped around the network with quadratic overhead (i.e. the message gets larger, increasing arrival latency), and therefore, likely adds more room for timing games.

In summary, timing games on Monad are possible and will favor sophisticated validators. While profitable for this subset, they in expectation reduce the block value of the proposers succeeding them, via excess transaction capture. Timing games are geographically centralizing by reducing the network visibility of nodes in distant locations, which reflects in inaccurate timeout votes, and a loss of influence to high performing low-latency hubs.

The financial industry has long grappled with the inefficiencies of traditional systems, namely settlement delays, restricted market access, and capital inefficiencies. Decentralized finance (DeFi) would eventually emerge as a response, but early implementations often fell short, plagued by issues like over-collateralization and limited composability.

Recognizing these challenges, Injective introduced iAssets - programmable financial primitives that facilitate enhanced liquidity allocation, position-based exposure, and cross-market composability. Unlike their static predecessors, iAssets are dynamic, on-chain instruments, with second-order utility and no pre-funding constraints. With iAssets, Injective aims to move blockchain-based stocks, commodities, and more beyond proof-of-concept, ushering in the era of Stocks 3.0.

The Evolution of Financial Assets – TradFi, Early DeFi, and the Emergence of iAssets

Traditional Finance (Stocks 1.0)

Traditional financial systems operate within structured, yet inflexible frameworks, characterized by delayed settlements (typically T+2), stringent access barriers, and segregated liquidity. The opacity of processes such as prime brokerage and rehypothecation further compound systemic risks, creating inefficiencies and restricting market participation to predominantly institutional actors.

Early DeFi & Synthetic Assets (Stocks 2.0)

The initial wave of DeFi introduced tokenized and synthetic assets, allowing for asset programmability and a more open financial environment. However, these models often required excessive collateralization (often surpassing 150%), leading to substantial capital inefficiencies. Liquidity pools were isolated, limiting the effective deployment of capital, and creating vulnerabilities such as liquidation cascades during market volatility.

Injective's iAssets (Stocks 3.0)

Understanding the shortcomings of both traditional systems and early blockchain solutions, Injective's iAssets introduce significant innovations to further the utility of on-chain assets. Key advancements include:

Composability: iAssets are fully integrated across multiple financial applications within the Injective ecosystem.

Capital Efficiency: Eliminating the need for excessive collateralization or pre-funded positions.

Dynamic Liquidity Management: Real-time liquidity provisioning aligned with market demands.

These characteristics mark a distinct shift from representational to programmable finance. Rather than merely mirroring the value of off-chain assets, iAssets transform them into composable building blocks—financial primitives that can be deployed across lending protocols, used as collateral, integrated into structured products, or programmed into hedging strategies. The result is a framework that not only preserves the core utility of traditional assets, but enhances them with real-time liquidity, seamless market integration, and systemic transparency.

In this light, iAssets are not just an iteration on previous tokenization efforts, they are a redefinition of what it means to own and utilize assets in a digitally native financial system.

Injective’s Modular Architecture – The Backbone of iAssets

Injective's iAssets are realized through a robust and meticulously designed technical infrastructure. At its core lies Injective's modular architecture, which has been developed over several years to support high-performance decentralized financial applications.

Exchange Module and On-Chain CLOB

The Exchange Module serves as the foundation for iAssets, providing a fully decentralized, on-chain central limit order book (CLOB). Unlike traditional automated market maker (AMM) models, the CLOB facilitates tighter spreads and more efficient price discovery. This architecture allows for professional institutions to dynamically manage liquidity, ensuring that iAssets benefit from deep and responsive markets.

Moreover, the Exchange Module plays a pivotal role in optimizing liquidity across the Injective ecosystem. By enabling a shared liquidity environment, it allows for seamless capital flow between various financial applications, including trading platforms, and structured financial products. This interconnectedness ensures that liquidity is not siloed, and instead dynamically allocated based on real-time market demands.

And iAssets haven’t wasted any time in picking up steam. Injective now hosts all Mag 7 stocks, which have done a cumulative $165M+ in trading volume since launch. iAssets as a whole have seen over $465M in trading, laying the foundation for a burgeoning asset category and aggressive innovation. And if that wasn’t enough - one particular asset of note really takes center stage, TRADFI, which achieved approximately $14 million in trading volume on its first day of listing.

Modular Design and Multi-VM Support

Injective's architecture is composed of interoperable modules, each serving a specific function within the ecosystem. This modularity gives developers access to a robust set of pre-built components, such as the Oracle Module, RWA Module, automatic smart contracts and more, without the need to build from scratch. For all Injective modules, click here. Furthermore, Injective supports multiple virtual machines (VMs), enhancing the flexibility and scalability of applications built on the network.

To learn more about Injective modules, click here.

Future Developments and Innovations in iAssets

And Injective isn’t stopping there. The team is actively working on several initiatives aimed at enhancing capital efficiency and utility, notably, their Liquidity Availability Framework.

Liquidity Availability Framework

One of the key developments is the introduction of a "Liquidity Availability" framework. This initiative seeks to optimize capital utilization by allowing liquidity to move dynamically between applications based on demand. While underutilization is a notable concern, the primary objective of liquidity availability is to address limitations brought about by application-specific liquidity, and ensure that liquidity is allocated more efficiently across the ecosystem.

Want to learn more? Check out Injective’s research paper on Liquidity Availability here.

Redefining On-Chain Asset Utility

Injective’s iAssets represent a pivotal advancement in the evolution of financial markets, transitioning from static representations to dynamic, programmable financial primitives. By addressing the limitations of both traditional finance and early decentralized finance models, iAssets offer enhanced capital efficiency, real-time liquidity, and seamless composability across financial applications.

Leveraging Injective's robust modular architecture and on-chain central limit order book, iAssets facilitate a more integrated and efficient financial ecosystem. This infrastructure not only accelerates development timelines but also fosters innovation, enabling complex financial instruments to be constructed with greater ease and reliability.

As the financial industry continues to evolve, Injective seeks to provide the foundational infrastructure necessary for the next generation of programmable finance.

Want to learn more about iAssets? Check out the iAssets research paper here.

Chorus One: Empowering the iAssets Ecosystem

As a leading institutional staking provider, Chorus One is proud to support the Injective ecosystem and its innovative iAssets framework. By operating a highly secure and reliable validator node on Injective, Chorus One ensures network stability and contributes to the seamless functioning of the Injective ecosystem.

.png)

.png)