We would like to extend our congratulations to Monad on the successful steps toward its mainnet launch – a milestone that marks the beginning of a new era for high-performance, Ethereum-compatible infrastructure. As the ecosystem prepares for this next chapter, we are excited to announce a new integration with Bitget, one of the world’s leading universal exchanges (UEX), to make Monad (MON) staking accessible to users across global markets.

This collaboration brings together Monad’s breakthrough execution architecture, Bitget’s global reach of 120M users, and Chorus One’s institutional-grade staking expertise, creating a seamless, secure, and highly scalable gateway for early participation in the Monad network.

Why This Integration Matters

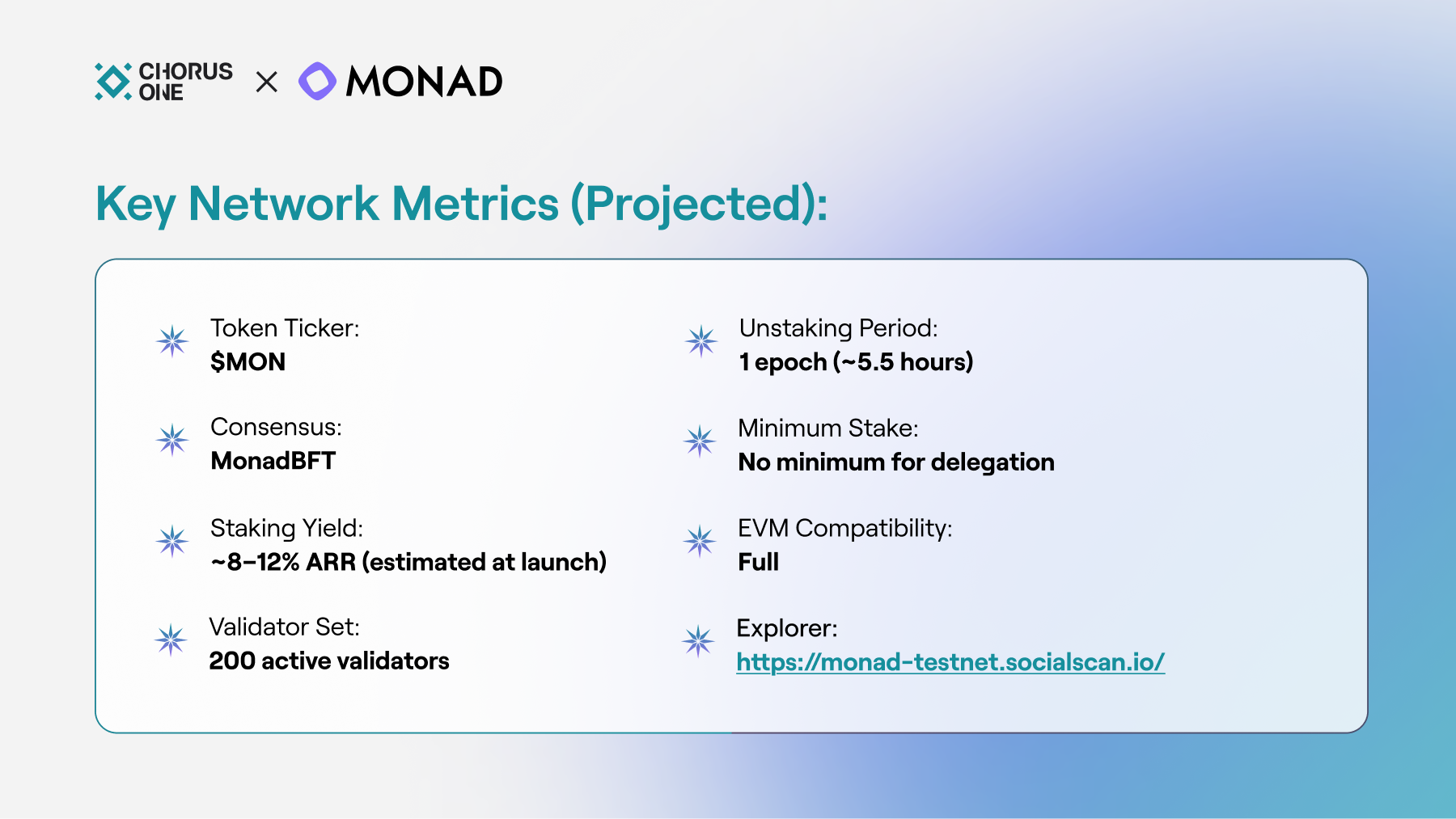

Monad’s design introduces a leap in execution performance, pairing parallelized transaction processing with MonadBFT consensus to deliver low-latency, high-throughput computation while maintaining full EVM compatibility. As anticipation builds for mainnet, demand for safe, transparent, and reliable staking pathways continues to grow.

However, during Monad’s initial phase, direct staking will be limited, and access will occur primarily through trusted partners. This is where the Chorus One and Bitget integration plays a critical role: it ensures that users can enter the ecosystem through an interface they already trust, backed by infrastructure built for institutional reliability.

What Users Can Expect

Through this integration, Bitget users will gain access to MON staking via Chorus One’s validator infrastructure, benefitting from:

1. A Secure Staking Pathway at Launch

Bitget will route staking operations to Chorus One’s infrastructure, ensuring that delegators participate through a highly resilient validator with a multi-year track record of zero slashing events across 40+ networks.

2. Clear Visibility Into Rewards and Operations

Staking rewards will be displayed directly within Bitget’s interface, offering a streamlined experience for users who prefer not to manage on-chain delegation flows themselves.

3. Support for Manual Compounding

As Monad does not auto-compound staking rewards, users will have the option to manually compound earnings through Bitget’s interface or other integrated tools. This gives full control over reward management while preserving opportunities for optimized yield strategies.

4. Global Accessibility

With Bitget’s strong presence in APAC, Europe, and emerging markets, the partnership ensures broad accessibility to MON staking from day one, especially for users who may not otherwise have access to early delegation options.

Complementing the staking integration, Bitget has also launched the MON On-Chain Earn product on November 30. This offering provides users with an accessible way to participate in Monad’s on-chain economy. Users can easily join through Bitget’s dedicated On-Chain Earn interface and start earning on their MON holdings. Click here to join the campaign now!

Chorus One’s Role in Enabling Institutional-Grade MON Staking

At Chorus One, our mission is to empower participation in next-generation decentralized protocols through:

- Highly reliable validator operations (over 99.9% uptime across testnets and mainnets);

- Robust risk-mitigation frameworks backed by Chainproof and MunichRe insurance layers;

- Comprehensive tooling including SDKs, dashboards, and API integrations for partners;

- Research-driven ecosystem support including analysis on Monad MEV, timing games, and validator dynamics.

For the Bitget integration, we provide infrastructure with continued monitoring, optimization, and reporting to ensure a smooth delegation experience as the ecosystem matures.

Strengthening the Monad Ecosystem Together

Bitget’s influence as a global universal exchange, combined with Chorus One's proven validator track record, helps strengthen the foundation of the Monad network even before its full launch. By lowering the barrier to entry and offering a compliant, scalable on-ramp, this integration helps ensure the validator set grows in decentralization, stability, and geographic diversity.

And as Monad prepares to introduce its high-performance EVM to the world, expanding staking accessibility is a crucial part of building a resilient and secure network from day one.

Looking Ahead

Monad’s arrival represents a transformative moment for the EVM ecosystem, delivering performance gains without sacrificing compatibility or developer experience. The integration between Chorus One and Bitget is only the first step in a long-term commitment to supporting the network with high-quality staking infrastructure, research insights, and ecosystem collaboration.

We’re proud to contribute to Monad’s journey, and equally proud to help users around the world participate safely and effectively in its early stages.

If you’re a platform, wallet, or institution looking to enable MON staking, our team is ready to support your integration.

Contact us to learn more about partnering with Chorus One for Monad staking.